Call it the revenge of the safe asset. Bonds, especially on the long-end, continue to see a sell-off on a surge in inflation and the continued view that the Fed will not change their rate hiking program. This decline has been coupled with generally weaker performance in equities which has led to higher correlation between equity and bonds. The correlation measurement, which is backward-looking, still is negative between stock and bonds but it has risen from previous lows. This increase reduces the “safety” effect associated with bond diversification which has been the “free lunch” for many investors. This will be a growing problem if it continues. Investors will have to make portfolio diversification changes.

The continued view that the Fed will raise rates is starting to impact international markets which have declined on a stronger dollar which has surged since the middle of the month. The combination of Fed tightening and other central banks continuing to follow easing policies has created a clear dollar yield advantage that is starting to affect capital flows.

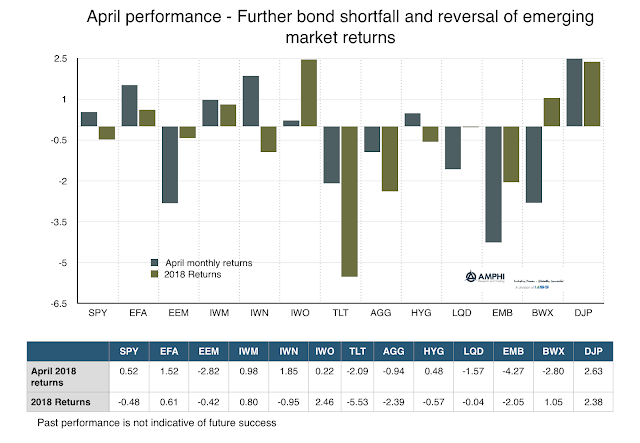

Equity markets were generally positive but showed mixed directions. First, economic growth was slower for the first quarter even though earnings were attractive. Second, long rates hitting the magical three percent mark has created some negative sentiment. That said, value proved to be a winner in April. Credit provided a cushion against some of the Treasury sell-off and commodities proved to be a winner based on higher energy prices.

The headwinds against a diversified portfolio are still the combination of higher inflation and a Fed that will continue to push borrowing costs higher. However, these expectations should already be embedded in expectations. Generally, there is not enough evidence to reverse a risk-on sentiment view but any further diversification should come through strategies and not through building further exposure in the “safe” asset.