A focus of global macro investing is looking for general factors which can have an impact across markets and countries but are displayed slowly in cross-asset relationships. Macro traders watch closely global and local financial conditions such as monetary liquidity as good indicators for potential switches between risk-on and risk-off environment. They also look for changes in credit conditions as a signal of potential shocks across local financial markets.

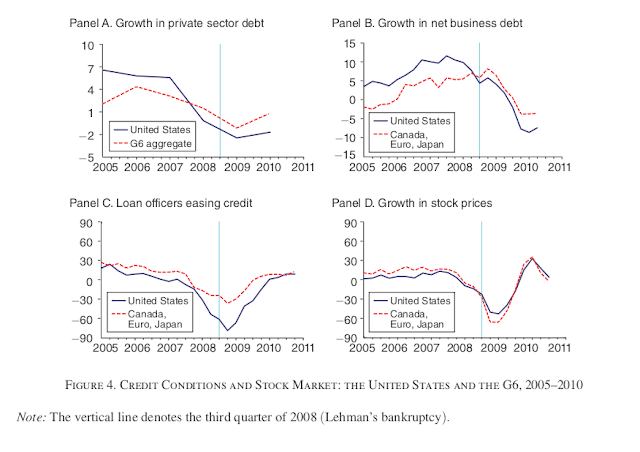

Research has found that the Financial Crisis was worsened by the high level of international synchronization especially in credit growth prior to the fall in 2008. The large fall in real and financial activity that was related to a global liquidity shortfall.

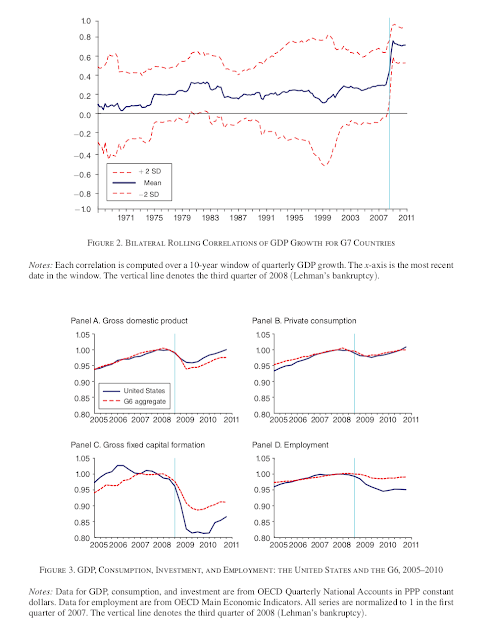

Liquidity shortfalls will have not only real effects but also impact investor and consumer sentiment. Tightening credit spills over to investor pessimism. (See Fabrizio Perri and Vincenzo Quadrini “International Recessions” American Economic Review 2018, 108(4-5): 935–984.) Their charts of the Financial Crisis show the growth correlation between G7 countries and the similarities in macro behavior. What is clear is that the high correlation was preceded by the downturn in credit markets.

Financial integration means that local liquidity shocks may have less impact because capital can flow from other sources, but when there is a global crisis the impact will be more synchronized and severe. Hence, following global liquidity is key to tracking potential tail risks in financial markets. Financial integration means that we get less diversification from holding international equity and bond positions. When there is a negative shock, investors are nothing to get the diversification desired or expected.

While following the Fed is a necessary starting point for global liquidity monitoring, the behavior of all large central banks have to be integrated to get a good picture of global liquidity. The integrated approach means that Fed rate rising has not spilled-over globally because other central banks are continuing to provide liquidity. The current key liquidity consideration is what will be the actions of the ECB, Bank of Japan, Bank of China, and Bank of England.