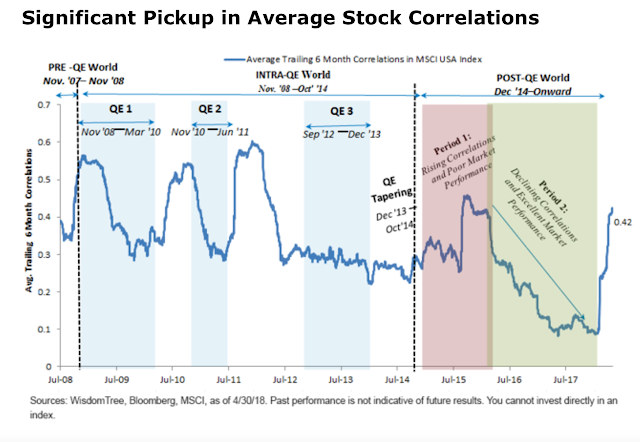

The average correlation across stocks (intra asset class) has important implication for portfolio construction and for active management. The chart below from Wisdom Tree shows average stock correlation since the Financial Crisis. It has been subject to sharp increases followed by declines. Our general view, consistent with this data, is that if there is a single factor macro event, there will be a corresponding increase across all stocks.

There is a an ebb and flow of macros events which affect the amount of any factor explaining stock variation. It does not have to be a negative event. There has to be a singular event that is perceived to impact all stocks. QE1 and QE2 were these types of singular events. The Taper Tantrum was another as well as the anticipation of the end of QE. Finally, the volatility shock of February 2018 was the most recent and perhaps the most severe. Events that will affect all stocks will increase average correlations.

The need for hedging and for global macro investing is increased when these correlation shocks occur. If an investor is on the right side of these shocks, which could either lead to higher or lower prices, it is profitable. If an active investor has built a diverse portfolio and is on the wrong side, performance will suffer. (Ongoing research is trying to match the changes in correlation with hedge fund performance.)

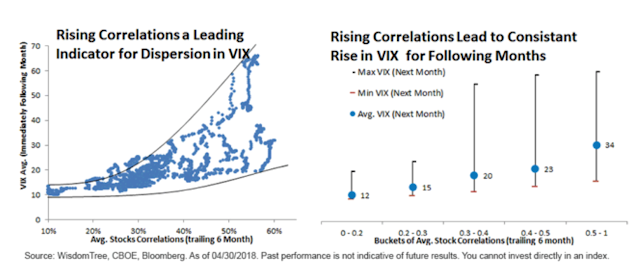

It is clear that when correlation goes up across stocks there will be a corresponding increase in implied option volatility for stock indices. There is less stock diversification within the index, so there is a impact on the index volatility. Additionally, the uncertainty and its resolution concerning a macro event will add to the overall index volatility.

There is a need even for stock pickers to have a macro view or have an appreciation for the changing correlation from macro events. For portfolio construction, picking alpha generator managers within equities may lead to heightened risk from correlation spikes. This risk requires diversification in to strategies that may focus on macro events.