HFR, the hedge fund index provider, announced a new set of indices based on alternative risk premium strategies generated from banks. This is a significant advancement in transparency for investors and shows the strength of this growing investing sector.

ARP has mainly been the domain of hedge funds. However, that has changed over the last few years as banks have increasingly offered a wide range of total return index products based on rules that describe specific alternative risk premiums. Bank products now compete directly with hedge funds and provide risk-premium strategies with low costs, transparency, leverage, and liquidity. The battle between banks and hedge funds is on.

Investors now have an enhanced number of choices. They can buy hedge funds as bundled risk premium products with a manager adding their skill and allocation expertise or buy a set of swaps to replicate specific risk premiums as generic return generators and use their skill at building the portfolio. The core question is simple. Do you need a hedge fund to provide these risk premiums, or can you obtain them from banks as index wholesalers?

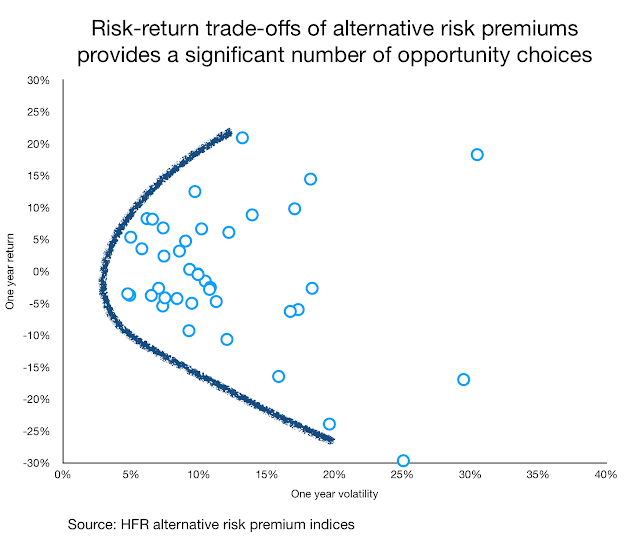

The chart above shows the 1-year return and risk for the risk premium indices offered by HFR, each a weighted average of similar ARP indices provided by different banks. All of the indices did not generate gains in the last year. Many showed that ARP investing over the last year was difficult, especially in the volatility strategy space; nevertheless, there have been many positive returning ARPs with reasonably low volatility. These ARPs can form the basis of a well-diversified portfolio that can replicate the behavior of hedge funds. This is worth tracking, especially against hedge funds which have not performed as well as expected.