How many times have you gone to a pension fund or endowment and heard the phrase, “You will have to check with my consultant”, or “If my consultant hasn’t approved you, I will not invest”. Pension consultants are powerful in the money management industry. Without their blessing, it is hard to grow an institutional money management business. There is the assumption by many that they have special investment powers that allow them to conduct due diligence and ferret information on managers that cannot be achieved my most others.

It should be easy to prove their value added. Just look at the managers they pick versus the managers they reject. This should not be much harder to test than determining whether a manager is better than a benchmark. It is just an issue of collecting the information from the consultants and comparing against a set of benchmarks and peer groups. Some have done the work, and the results are available for all to see, (Investment Consultants’ Claims about Their Own Performance: What Lies Beneath? Gordon Cookson, Tim Jenkinson, Howard Jones, and Jose Vicente Martinez)

The answer is that their value added for picking managers is limited. Are their picks harmful? Perhaps not. But, paying them for their secret due diligence performance sauce is not going to get you much. Show them this study and just ask them to prove otherwise.

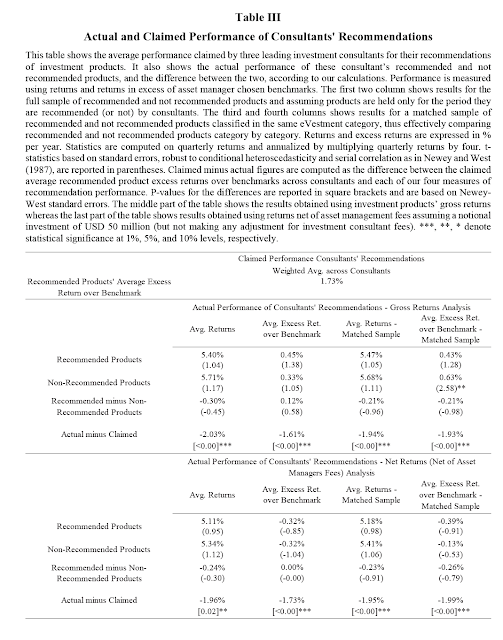

The study used a database of recommendations from the FCA for UK consultants some of which are the biggest in the world. This database has not been available to the public. The conclusions suggest that the consultant recommendations do not outperform non-recommended managers or benchmarks. These results are inconsistent with the claims of the consultants who show outperformance versus selected grouping for comparison. A close look at the methods used for consultant claims suggest that there may be biases in their methodologies.

This work scratches the surface and needs closer analysis for US recommendations and through using alternative methods for comparison, but the simple conclusion is that performance value-added through consultant manager picks has limited value.

Do consultants provide other value-added services? Helping with standardization of practices, doing operational due diligence and background checks, helping with performance benchmarking, forming strategic allocations, and providing data on sets of managers are all useful services. But, pensions may want to be more suspect with respect to using their picks for finding the best performing managers. Savvy pensions may have known this for years, but buyers beware.