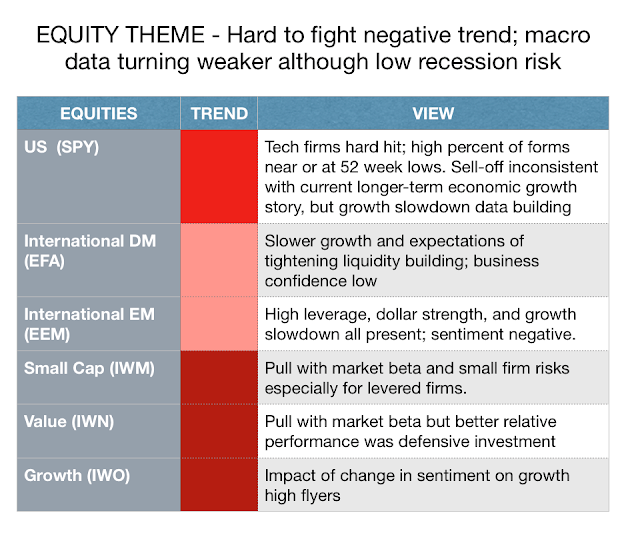

It not a matter of like or dislike the fundamentals of equities in the current environment. When sentiment changes and volatility increases, reassessment of current exposures is warranted. However, concern about the macro environment should be increasing. Maintaining lower market risk exposure by more than half of core allocation from 60% to 30% or half equity beta exposure is appropriate. (The darker red signifies a stronger trend.)

Growth – While recession risks are still limited by any probability-based model, economic growth will be tempered in 2019 both in the US and rest of world. Earnings have not yet been significantly affected by growth, but forward expectations are now slightly biased downward.

Liquidity – Continued Fed tightening and expectations of tightening around the rest of the world serve as a negative for fixed income. High rates are starting to impact higher levered firms and lending. Make no mistake this is what central banks want.

Risk Appetite – Higher volatility with changes in sentiment suggest market is moving to risk-off environment. Financial condition trends are pointed lower. With risk-off, harder to buy on dips so more downside follow-through.

Structural – Gridlock in government will negatively affect further tax reform and regulatory changes. Fiscal deficit is now pro-cyclical which will further affect rates.

Technical – There have been some key periods of divergence between equity style sectors. International and EM have actually been a place to hide in the near-term

Looking over year-to-date, six-month, and three-month returns shows three distinct differences: The divergence between US and rest of world, the dislocation between large-cap and value, growth, and small cap equities, and the reversal of the earlier international underperformance.

Related Posts

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

The Evolution of Trading from Systematic to AI

Is AI the next step in the evolution of trading? History proves new tools storm the markets, then high adoption erases their edge. What can futures trading history teach us about AI’s trajectory? The 1980s: Rise of Rules-Based Trading Building on simple regression models that aimed to identify patterns across sectors, the 1980s showed that […]