A big problem with macro fundamental investing is getting timely data on the economy and then translating that information to effective investment signals. Government issued data generally are out of date and old information for forward looking forecasts. Hence, there is greater value on macro data that is current and prospective.

The PMI forecasts, which are announced monthly, are a good macro candidate given they are measured across a broad number of countries, have significant history, and are forward-looking expectations of economic activity.

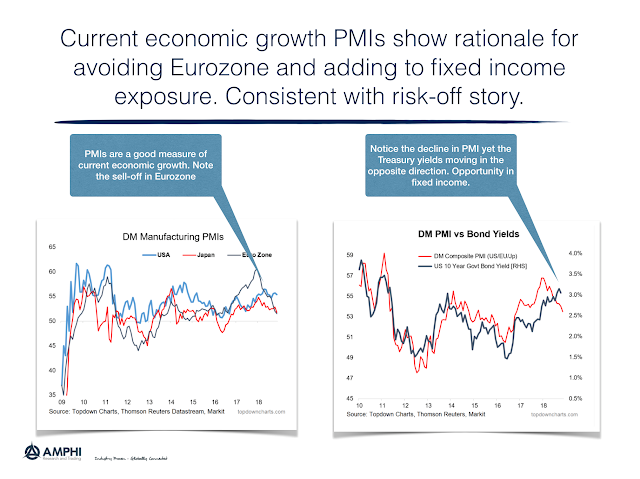

A graphically analysis of PMI explains the major sell-off in European equities relative to the US. It can also explain the decline in EM equity valuation. Similarly the PMI forecasts can tell us something about the broad trends in bonds. If the PMI is declining (increasing), there should be a bond rally (decline). Rates fall during declines economic activity. Investors just have to get an early signal. The current reading suggest that any switch away form equities should focus on bonds not cash.

After hundreds of discussions with hedge fund managers, I am still surprised that there is a fear of revealing investment processes under the assumption that someone will steal their ideas and intellectual capital. There are few investment styles that are truly unique and special. What is special is still strategy execution – the practical process of delivering returns. Skill is with the decision-making execution of information and strategy.

All hedge funds are not created equal as the return box chart shows for the post Financial Crisis period. There is a significant amount of dispersion across hedge fund styles. Over the period 2009-2018, the difference between the best and worst hedge fund category is almost 7 percent after we account for global equities and bonds.

The attraction to private equity and other less liquid alternatives is clear from the Guide to Alternatives by JP Morgan Asset Management. The return profile is much higher for private equity and debt funds than more liquid alternatives and global bonds; however, the dispersion in returns is multiples higher than what can be expected from other public categories.