The asset allocation decision for holding equities (risky asset) over bonds (safe asset) is inherently a macro decision. This macro decision is one of the most important asset allocation decisions given the large differential between stock and bond returns. The average annual difference is over 625 bps over the last 90 years in favor of stocks. However, bonds deliver lower volatility and reduce portfolio risk.

We have outlined a set of macro variables that determine the choice between stocks and bonds. Of course, the first thing to note is that there will always be a bias toward the risky asset. There is a 2/3rd chance that equities will outperform bonds on an annual basis over the last 90 years. Hence, from an asset allocation perspective the choice is not about stock or bonds but less equities and more bonds in an attempt to miss the large down moves.

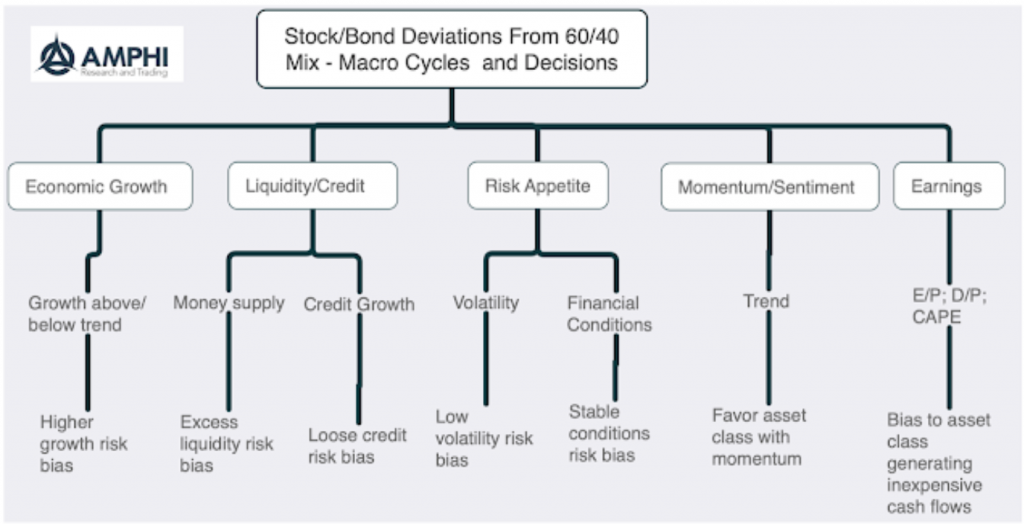

We focus on a few key decision choices:

- Growth – Above average or accelerating economic growth is equity positive.

- Liquidity/Credit – Increase in above trend money creation and expansion in credit is equity positive.

- Risk appetite – Low or declining volatility and improving financial conditions is equity positive.

- Momentum – Momentum is a key risk factor, so positive stock momentum should not be faded.

- Earnings – Overall stock earnings relative price informs investors on cash flow or carry from investments. Higher earnings, earnings per price, and dividend yield are equity positive.

Fundamental data can be mapped into a score for each of these macro factors. These macro factor scores can then be mapped into a weighting scheme between equity and bonds. The score to weighting map can be adjusted based on a level of risk tolerance. Low risk tolerance will have limited tracking error from the core 60/40 stock/bond mix while a more aggressive investor with higher risk tolerance will allow for more tracking error.

The overall allocation will be a function of the weighting of each macro factor. A higher weight to momentum will have more weight adjustments and variation. Economic growth, which does not change as frequently, will have less weight variation from month to month. More weight on the longer-term factors will have a slower speed of adjustment. Our current weights show a tilt to bonds even with the strong momentum in January based on growth fundamentals and the reality that a Fed pause is not Fed ease.