An ensemble approach to modeling can be an effective way to get a good idea of the consensus and differences in forecasts on futures moves in the Fed funds. This is an effective alternative to looking at Fed funds futures and options as a market estimate.

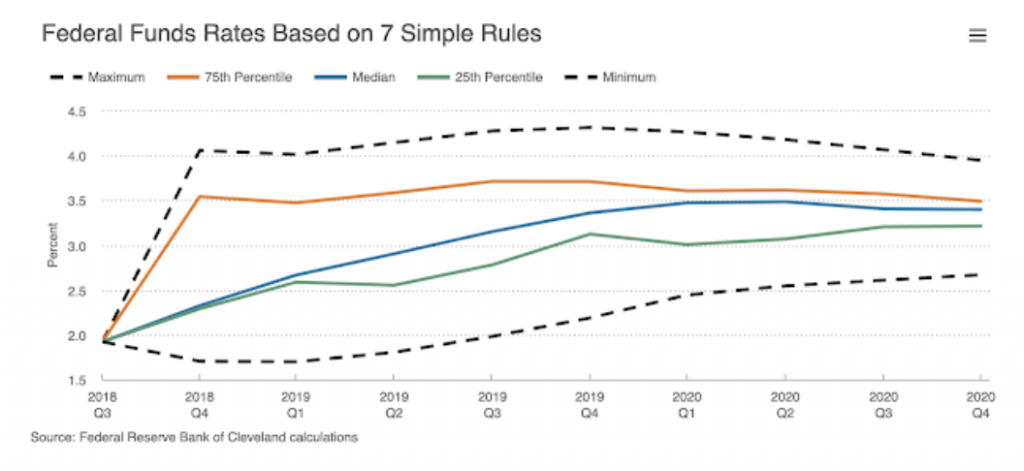

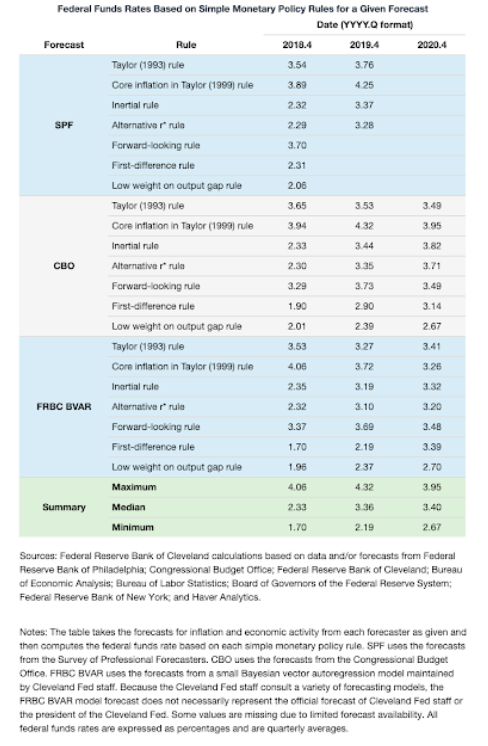

A nice place to show the impact of ensemble modeling is the Cleveland Fed research site which provides quarterly updates of Fed fund forecasts using seven different models. The next update is at the end of this month. The ensemble is developed through using some variations on Taylor Rules that are relatively easy to estimate and have done a good job in the past.

The approach is simple. The different forecast models are employed with different forecast assumptions. A nice benefit of this approach is that anyone’s forecasts can be used with the same set of models as a comparison. It is not the underlying assumptions that are compared but the forecast output through these standardized sets of models. While the Cleveland Fed updates this approach on a quarterly basis, model forecasts against current expectations can be done at anytime. You can call the differences model dispersion or uncertainty. All of these models have rational intuition, so the dispersion across models tells us something about underlying economic uncertainty.

By comparison to the last Cleveland estimates before year-end, we are in a new monetary world. 2018 is ancient history. We are currently between the 25 percentile and minimum forecast. Trading that range is the place of global macro opportunity. Currently, the entire range of forecasts will be lower and likely tighter.

Related Posts

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

The Evolution of Trading from Systematic to AI

Is AI the next step in the evolution of trading? History proves new tools storm the markets, then high adoption erases their edge. What can futures trading history teach us about AI’s trajectory? The 1980s: Rise of Rules-Based Trading Building on simple regression models that aimed to identify patterns across sectors, the 1980s showed that […]