Commentary by AG Capital Management Partners, LP

The Discretionary Global Macro Program generated a -4.1% return, net of fees, in September 2021, leaving YTD performance at -6.3%.

An Asian Inflection …

Newspaper headlines screamed that the ongoing collapse of Evergrande–China’s largest real estate developer with over $300 billion in debt–is the country’s “Lehman” moment. The implication is that it’s a crisis on par with the 2008 leveraged collapse of the U.S. banking system during the Great Financial Crisis (GFC). Catchy headlines like this were promptly forgotten two weeks later, given that there was no immediate contagion to the U.S. financial system via credit spreads or derivatives.

If forced to make stretched analogies with the GFC, a better one would be to compare Evergrande to Bear Stearns. Financial professionals who remember every moment of the lead up to the 2008 main event will recall that in July 2007, the Bear Stearns High-Grade Structured Credit Funds acknowledged in an investor letter they had lost between 90-100% of investor capital due to leveraged bets on subprime housing market debt. The housing market itself had peaked back in 2005. There was a two-year lag between the peak of the underlying asset (housing) and the first major warning sign with the implosion of these Bear Stearns hedge funds. And yet the grand finale, the September-October 2008 crash in equity markets and the Lehman event itself, did not occur until more than a year later.

Evergrande is a sign of what’s coming. It marks the end of China’s 15-20 year fixed asset investment model, where real estate now makes up 25-30% of GDP. President Xi Jinping has made it crystal clear that he intends to inflict short-term pain on the economy (real estate, tech monopolies) to set the groundwork for a needed rebalancing of the Chinese economy toward household consumer spending. This is a major, monumental inflection point of the sort that happens once a generation and will take 10-20 years to reach fruition.

Why is this important? Because our global economy is not just interlinked via supply chains that bring Chinese goods to the West, but also via capital and investment flows. What starts in China ends in Europe and the U.S. And the short-term pain China is administering to its economy will spread disinflationary and deflationary winds across the Pacific. That means lower orders for German machine tools. And weaker commodity demand. It also implies declining long-term interest rates, not just in China but globally, at least for the next 12-24 months.

… Ties into a U.S. Inflection

The timing of China’s decision to rebalance its economy coincides with several inflection points for asset classes. Here is our take:

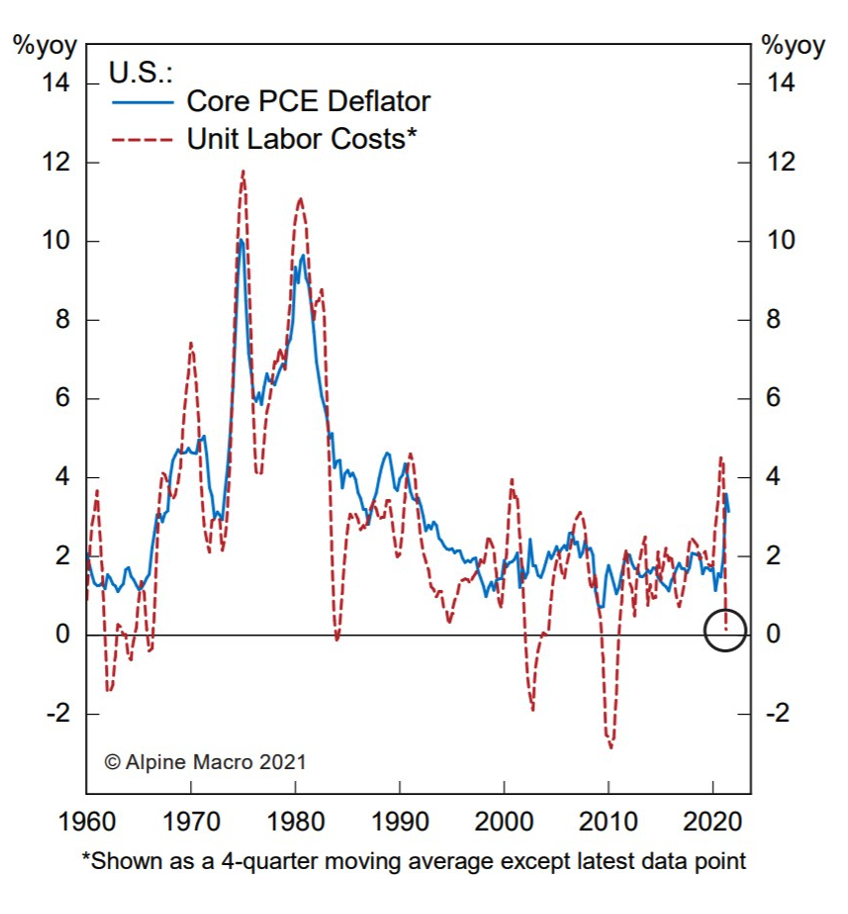

U.S. bonds: Most commentators view a headline inflation print of 5% and a 10-year Treasury at 1.4% and claim that the bond market is ‘crazy’. The bond market has always been considered savvier than the equity market, and does not care about inflation today, but about inflation each year over the next 10 years. And the bond market is telling you that the current inflation prints will not last. Not only because supply chains will inevitably be resolved, but also because wage inflation has fallen to near recessionary levels (chart below).

Extremely low unit labor cost prints occur at or near the beginning of economic downturns.

How is it conceivable that we could be on the cusp of an earnings recession, or even an outright recession? Simple: U.S. fiscal spending is about to go from a +$9 trillion response to the pandemic, back to a normal +$3 trillion, for a net contraction of -$6 trillion, all of which is spending power that is being removed from the consumer.

A negative U.S. fiscal thrust combined with a slowing engine of the global economy (China) implies that not only are bond yields unlikely to rise further, but they should continue to decline once the market’s near-term focus on the headline inflation panic abates.

U.S. equities: The long, slow bull market in equities that kicked off in March 2009 finally seems to be ending, after a parabolic, bubble-like move from the Covid-19 low in early 2020. In previous letters, we have made the case that the March 2020 low did not mark the beginning of a new economic cycle, but rather set the stage for the final push higher in the 2010s bull market. Forget about the old rule that -10% is a correction in equities and -20% marks a bear market. A true bear market makes its mark over time, taking 1-2 years to play out, and flushes out leverage, poor business models, and resets the economy for the next cycle. We believe the February-March 2020

Covid crash was no different than the summer 1998 Russia/LTCM crash–it just set the stage for the last 18-month push higher into the secular top of a great, long bull market.

If we are correct, and if equities are currently putting in a secular top, they may very well churn sideways for the next decade, intermixed with a couple of -30% or -40% bears markets, in order to work off the extreme valuation that they currently trade at, more expensive than the 2000 peak on all metrics other than a simple 12-month P/E.

Commodities: A lack of investment in base metals and in the energy complex is showing up with clear price rises in oil & gas and other extracted commodities. This lack of investment is compounded by an ESG mindset that has and will continue to prevent the needed investment to occur in traditional energy sources, which we will rely on for decades to come. We are bullish commodities for the next ten years. But we cannot be bullish here and now. What we have outlined above, in conjunction with a Bloomberg spot commodity index that is the most overbought in its history, leads us to believe that we are on the cusp of a 15-25% correction in most commodities on a 12-24 month horizon. After that, the path of least resistance is upward.

U.S. dollar: The dollar will be abused for the next decade as the Fed is no longer the sanctimonious institution it was perceived to be a couple of decades ago (can you imagine a U.S. Senator speaking about Greenspan the way Elizabeth Warren recently upbraided Powell? It would have been unfathomable and is a sign of the times). The Fed will be under political pressure to maintain negative real interest rates and to work with the U.S. Treasury to “re-allocate” capital toward social objectives and higher inflation targets. That is the big picture trend. But as with our view on commodities, the near-term offers the opposite, with tightening liquidity in the U.S. (Fed taper and a reduction in the Treasury General Account) leading to a stronger dollar into 2022.

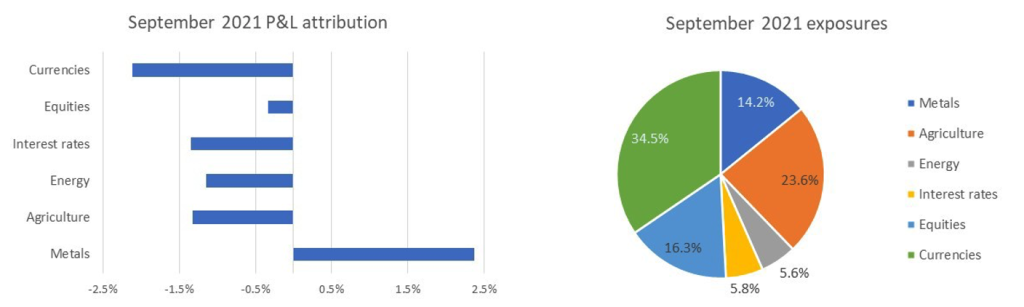

September performance and current portfolio

Performance in September was negatively impacted by our long bond position (per our thesis above), which we closed out at a loss as yields rose. We intend to reinstate this position in the weeks/months ahead. We also had a loss from our long Japanese yen position, which tends to correlate negatively with selloffs in equities and commodities, and as such lined up with our negative view toward those asset classes.

We currently are positioned long the U.S. dollar vs the British pound. The U.K. economy is suffering more from supply chain and energy shocks than other major developed markets, and as it appears to be on the brink of a recession, we expect monetary policy to ease in the U.K., hence our decision to use it to express our long dollar view. We are short copper, in line with our broad view on commodities, and short the Russell 2000 stock index, in line with our view of a secular top in equities. A long coffee position rounds out our portfolio and is predicated on the supply damage to Brazil’s crop from a back-to-back drought and frost.

Trading futures involves substantial risk of loss and is not suitable for all investors. Past performance is not necessarily indicative of future results.

Related Posts

Navigating Economic Crossroads: A Closer Look at the Unconventional Path

In the famous Robert Frost poem “The Road Not Taken,” two paths diverged, and he took the one less traveled. We can look at charts of the US economy and compare them to previous periods to see that so far, we are taking the less traveled path as well. It makes all the difference. Despite […]

Cargo Collapse Chronicles: Navigating the Economic Storm through Freight Industry Signals

Economists often look for the proverbial “canaries in the coal mine” to predict where we head next. Specific areas of the economy tend to presage slowing growth earlier than others. The shipping of materials from one place to another is one such area. A supply chain is either gearing up for future sales or reducing […]

Ag Market Update: Wheat Prices Drop, China Becomes Top Wheat Importer, and Soybean Complex Dynamics

Commentary provided by Chad Burlet of Third Street AG Investments For corn and soybeans, it was a quiet harvest month as far as prices were concerned. Futures contracts for both crops had only 5-7% trading ranges and settled within 1% of where they were a month ago. The U.S. harvest is progressing well, with both crops ahead […]