For many investment strategies, the difference between a good and a bad manager is based on their ability to manage risk. It is as much about how volatility is handled as return generation. A good strategy that does not manage risk well will never be successful.

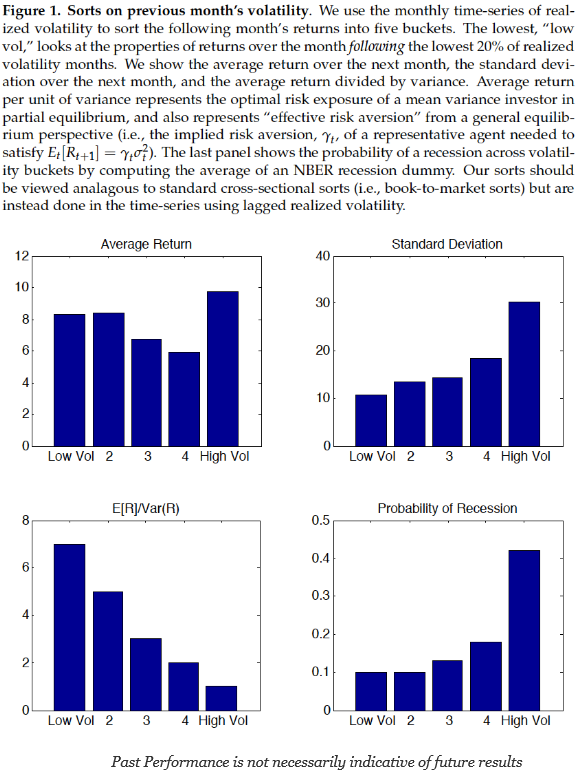

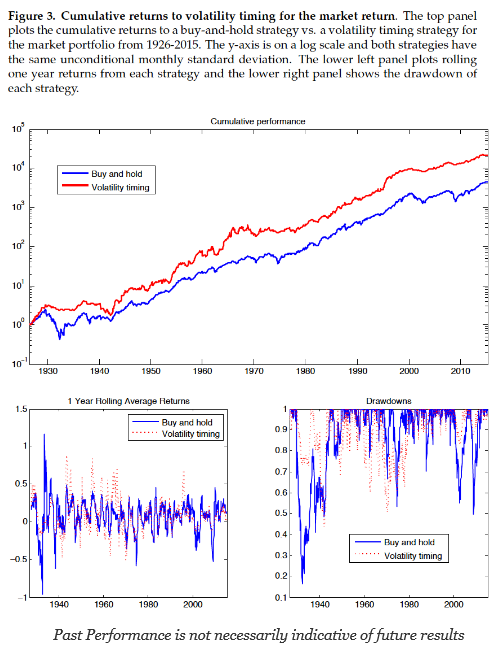

A key conclusion from a recent paper that focuses on volatility and factor management shows that controlling volatility provides a significant enhancement for many factor-based strategies. If you control volatility, you will get a positive bump in return to risk ratio.

This is at odds with the conventional wisdom of some in finance who believe you must be in the market during risky periods like a recession to gain extra return. You get paid to take risks during periods like a recession. This new research says that it does not matter when you invest in the business cycle. Managing risk will improve performance, and that means cutting exposure when volatility is high. Timing market volatility will help any investment strategy because volatility is generally independent of return. Put differently, if you control the risk, you will be better off versus a simple buy-and-hold for a given factor exposure.

This is all explained clearly in the paper “Volatility Managed Portfolios” by Alan Moreira and Tyler Muir. Their approach to volatility management is very straightforward, which makes their conclusions so powerful. The authors scale exposure by the inverse of conditional volatility while focusing on the classic Fama-French factors and carry. Since volatility is a persistent variable but not highly predictive of excess returns, managing or timing risk is not closely associated with the factors driving returns.

The importance of this paper is evident once it is read in its entirety. The authors carefully address many of the concerns readers may have and test the hypothesis from several perspectives. While the enhancement from volatility management is not strong in all cases, the weight of the evidence suggests that volatility management is a key way for managers to enhance return to risk.

The real market skill for many managers may be with their timing of volatility and not returns. Cutting (raising) exposure at higher (lower) volatility periods seems to be a proven strategy for alpha generation and Sharpe ratio increases. This research supports a comment I have often used, “I would only charge 75bps for a simple trend-following model but 125 bps and a 20% incentive fee for the risk management.”

(Hat tip to Peter Golger for pointing me to this paper.)

Photo by Weston MacKinnon on Unsplash

Related Posts

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

The Evolution of Trading from Systematic to AI

Is AI the next step in the evolution of trading? History proves new tools storm the markets, then high adoption erases their edge. What can futures trading history teach us about AI’s trajectory? The 1980s: Rise of Rules-Based Trading Building on simple regression models that aimed to identify patterns across sectors, the 1980s showed that […]