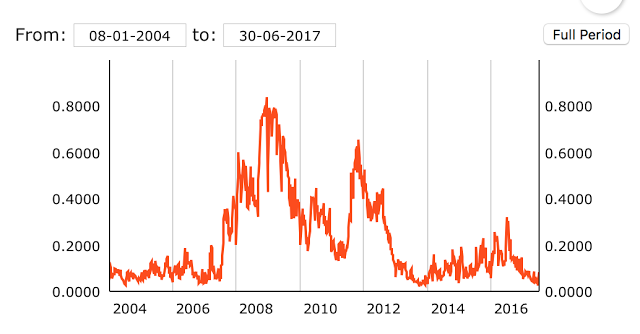

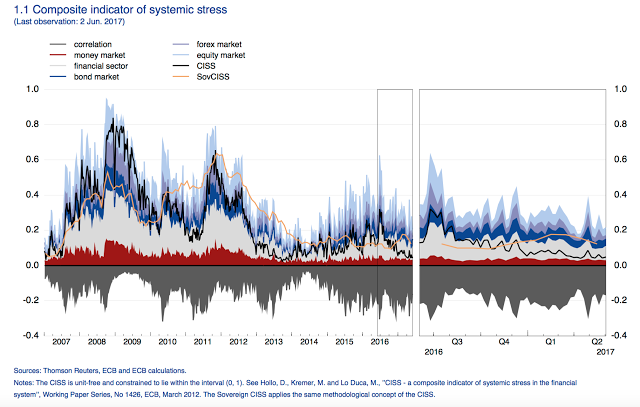

Don’t worry, be happy and without stress. The ECB Composite Index of Systematic Stress (CISS) measures declining stress in the EU. While there is a big disclaimer with the ECB risk dashboard that this is not an early warning system, the declining trend tells a story of stability.

This index serves as a European equivalent of the stress indicators used by the Federal Reserve Banks; however, there is a greater emphasis on cross-claims country claims, flows, and banking risks. The CISS numbers tell us that Euro area stress has been less volatile and reached all-time lows after spiking during the BREXIT vote. The US stress indices have also been trending down in 2017. This downtrend is consistent with EU equity volatility measures.

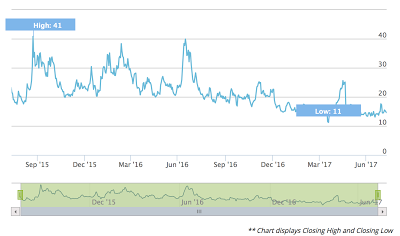

The VSTOXX volatility index below has shown a consistent downtrend, albeit there have been spikes that suggest liquidity may be strained in equity markets at times.

These positive stress numbers should influence the ECB. A tapering of bond purchases would seem natural given the current state of stress, the lowered deflationary fears, the lower unemployment in most countries, and positive growth. A tilt to a policy change seems appropriate. Unfortunately, global macro managers who often thrive on stress and market dislocations have not fully taken advantage of this less stressful environment.

Related Posts

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

The Evolution of Trading from Systematic to AI

Is AI the next step in the evolution of trading? History proves new tools storm the markets, then high adoption erases their edge. What can futures trading history teach us about AI’s trajectory? The 1980s: Rise of Rules-Based Trading Building on simple regression models that aimed to identify patterns across sectors, the 1980s showed that […]