As measured by a well-watched peer group index, the managed futures hedge fund strategy is in a significant drawdown. Despite this, money is still flowing as investors have taken a forward-looking view of what this strategy will do if there is a sell-off in major asset classes like equities.

Of course, indices do not represent the behavior of individual managers within this space. Some winners and strategies have made money over the last two years. It is just that the search may be a little more complicated because many big names which focus on longer-term trends in financial markets have had fewer profitable opportunities. Generally, better-diversified managers across style, timing, and markets have done better.

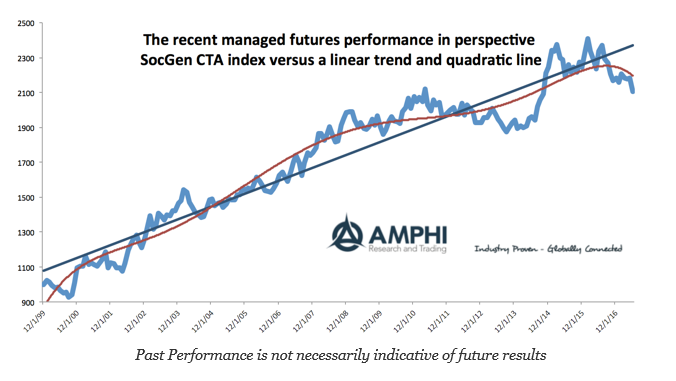

Our first chart shows the value of the SocGen CTA index since inception with a trend and quadratic line fitted through the index values. There was a clear fall below the trend in 2016, which has accelerated.

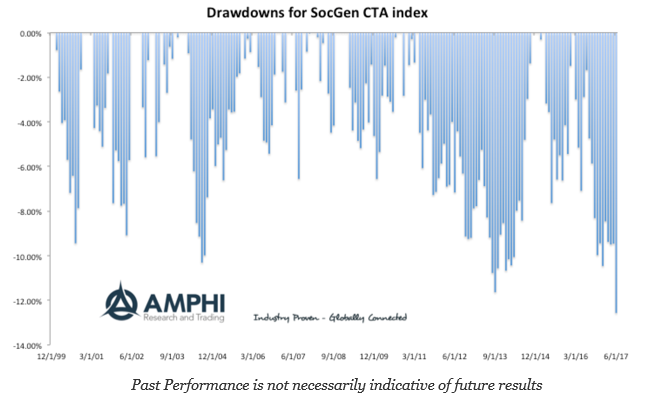

The actual drawdown is at an index maximum beyond 12%. There have been 10% plus drawdowns in the past; however, those have been in periods of higher market volatility. A quick analysis shows that the amount of time spent at high water marks is usually low, about 20% of the months, and the amount of time beyond a 7% percent drawdown is also low at about 20%. So getting to this drawdown was not unusually fast, but the last year has shown a strong trend.

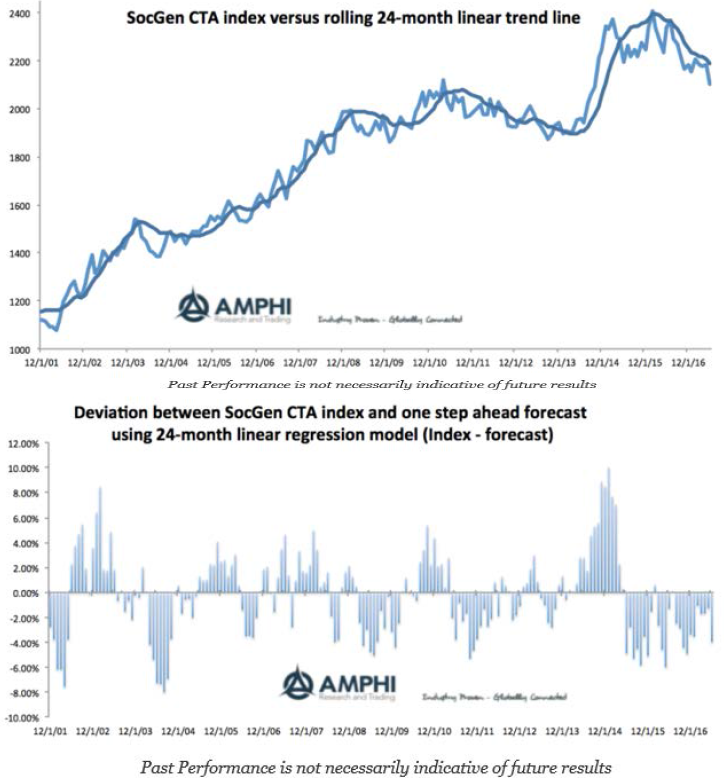

We also looked at the index using a rolling 24-month linear trend model which provides some deeper visual insight on the current down trend. It is steep with the inflection point in early 2016. The one step ahead forecast from the linear trend can be used to see how managed futures have deviated from recent trend. The data show that the current poor performance has been much stronger than the down trend and unusual relative to past linear forecasts.

For those that have invested in managed futures, the last eighteen have been challenging. Still, from a forward-looking perspective, the likelihood of a disruption in equity or bond markets has increased, and the possibility of a further drawdown based on current strategy volatility is lower. Drawdowns are path dependent. Hence, the past history is relevant yet expectations of potential market turbulence may be more important for current allocation decisions.

Related Posts

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

The Evolution of Trading from Systematic to AI

Is AI the next step in the evolution of trading? History proves new tools storm the markets, then high adoption erases their edge. What can futures trading history teach us about AI’s trajectory? The 1980s: Rise of Rules-Based Trading Building on simple regression models that aimed to identify patterns across sectors, the 1980s showed that […]