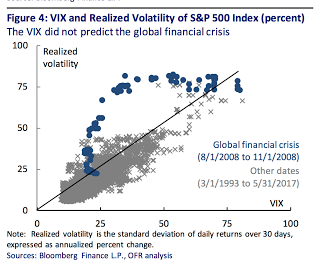

A provocative chart from the research piece The Volatility Paradox: Tranquil Markets May Harbor Hidden Risks by the Office of Financial Research Markets Monitor shows the poor forecasting of volatility when there is a regime change. Of course, tranquil markets harbor hidden risks. Low volatility is pricing in a lack of imagination of what the future may hold. The markets usually say that tomorrow’s change will be represented by the deviations of yesterday. We have learned from reading Minsky that low volatility will lead to risk-seeking behavior as investors reach for yield, employ leverage, and become complacent. Hence, a shift in regime will lead to more dramatic change in volatility.

Nevertheless, the most telling part of this chart is that when the big transitions come, the VIX index will not fully anticipate the move and realized volatility will move faster than the market’s ability to discount regime change. When market volatility reverses, the move is swift, so asset allocations for these types of events have to be structured today and not when the event is occurring. The cost for preparing a defensive diversified portfolio is the potential performance drag waiting for a big market reversal.

Related Posts

Anatomy of a Tough Month for Trend-Followers: Tariff Shocks & Volatility Spikes

It is often said that trend followers provide “crisis alpha.” This means that market stress often benefits their strategies. This follows logically as moves get larger, coordinate together, and run consistently, trading becomes easier. These managers quickly caution that they do not always provide this negative correlation. Price action can swing unpredictably against long-standing trends […]

Time-varying correlation – Diversification benefits are dynamic

What is the correlation between two assets? The correlation is critical because it is the driver for any diversification decision. The better question is, “What is the correlation now, and what can it be in the future?”. Correlations are often time varying and regime specific. In bad times, correlations rise, so the diversification expected is not present when you need it. This phenomenon requires more thinking about tail risks and how to best address them.

The “3 by 5 Index Card” on What You Need to Know About the February VIX Spike

University of Chicago professor Harold Pollack in an interview a few years ago mentioned that the best money advice can fit on a three-by-five inch index card. He was then challenged to write the card. His financial advice went viral. We follow this tradition by focusing on a simple “three-by-five index card” on the VIX volatility spike earlier the month.