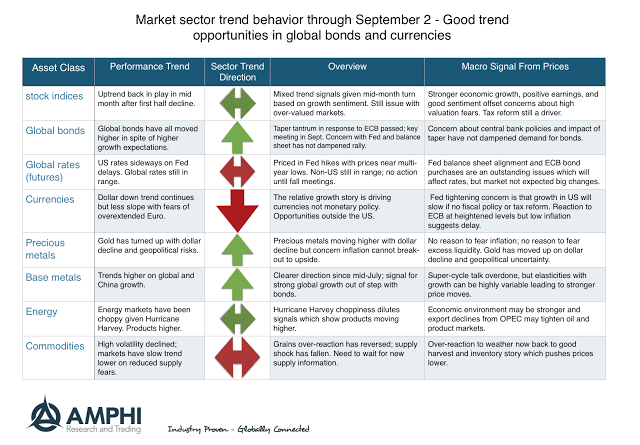

Many of our trend indicators were mixed coming into last month but continued gains in currencies and a strong bond rally positively contributed to performance for many CTA’s. The current trend indicators suggest continuation of these existing price moves. We take a representative sample of markets in a sector and count how many have up or down trends to form a sector estimate. The sector estimates can be strongly up or down or more neutral with a bias up or down as indicated by our arrows.

Stock indices sold-off earlier in the month only to rally during the second half on positive sentiment concerning tax reform and less aggressive Fed talk concerning its balance sheet. Bonds continue to move higher albeit with weaker slope. Currencies also continue their trends, yet the momentum against the dollar has slowed. Precious metal moves have been tied with currency trends. Energy markets have been affected by hurricane volatility and commodities are biased lower.

While some of the strongest trends last month may reverse, our general view is that trends often last longer than expected and without a policy or economic surprise, there is little reason to see a change.

After hundreds of discussions with hedge fund managers, I am still surprised that there is a fear of revealing investment processes under the assumption that someone will steal their ideas and intellectual capital. There are few investment styles that are truly unique and special. What is special is still strategy execution – the practical process of delivering returns. Skill is with the decision-making execution of information and strategy.

All hedge funds are not created equal as the return box chart shows for the post Financial Crisis period. There is a significant amount of dispersion across hedge fund styles. Over the period 2009-2018, the difference between the best and worst hedge fund category is almost 7 percent after we account for global equities and bonds.

The attraction to private equity and other less liquid alternatives is clear from the Guide to Alternatives by JP Morgan Asset Management. The return profile is much higher for private equity and debt funds than more liquid alternatives and global bonds; however, the dispersion in returns is multiples higher than what can be expected from other public categories.