HFR has announced a new set of risk parity indices. The set of indices includes risk parity strategies at different volatility levels and for both institutional levels and smaller funds. These investable indices represent 25 different products with $110 billion in AUM. The risk parity portfolios are generally comprised of four sectors which are given equal risk weight: equities, credit, interest rates, and commodities.

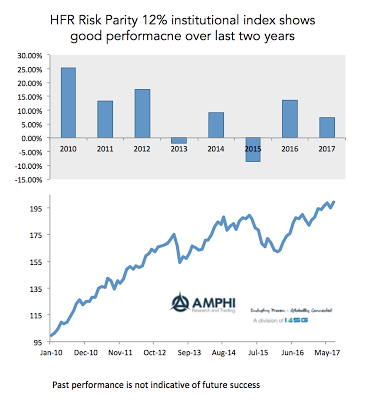

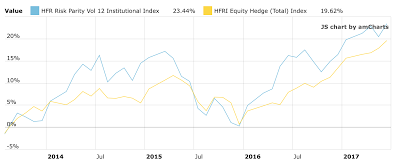

The result of equal risk weighting will be a stronger allocation to bonds versus stocks given the lower volatility of bonds versus equities. Clearly, periods of strong bond performance will lead to outperformance versus even an equal dollar-weighted stock/bond portfolio. Nevertheless, the last two years have shown strong positive returns after a disastrous 2015. These indices have done better than a broad-based equity hedge fund index and may again be worth looking at as a systematic investment alternative.

These indices may be another way of expressing a systematic approach to portfolio management relative to global macro and managed futures. You might initially think that risk parity and global macro or managed futures has little in common with risk parity, but there are some structural similarities which make a comparative analysis reasonable.

Many global macro and managed futures programs use some form of volatility targeting which is consistent with risk parity approaches. Additionally, systematic managed futures will often risk weight sectors with exposures in equities, bonds, commodities, and foreign exchange. The largest differences is with the core holding of credit versus foreign exchange exposure as a sector and the active determination of directional positions either long or short versus passive risk exposures.

The risk parity approach was discredited by many based on the poor 2015 performance but it actually did what was expected during that period, albeit not what was wanted. It is now doing what is expected, offering equal risk-weighting across a well-defined set of sectors. It may serve as an alternative for investors who want a systematic approach to risk management but without any directional market views.