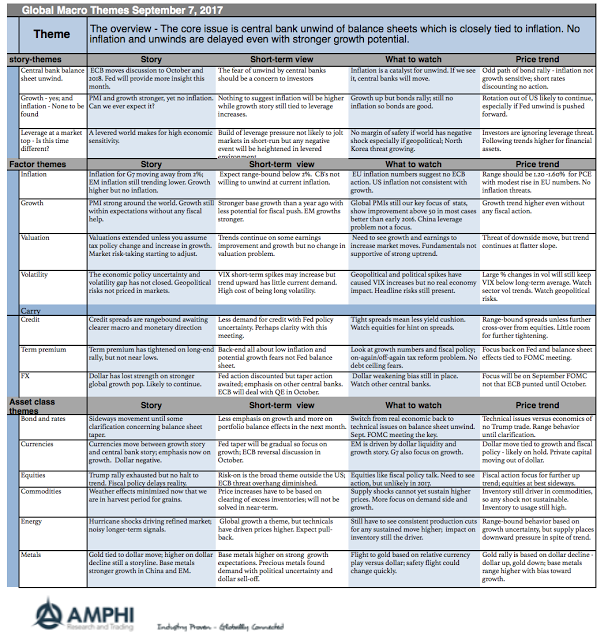

Where is that inflation? Central banks have this fixation on 2% inflation as both a goal and a signal. Policies have been structured for the magic 2% and signals for balance sheet action are based on the inflation hitting 2%, yet current inflation has not been able to reach this number. Growth expectations have been moved higher, yet there seems to be continued economic slack that will not allow product prices to push beyond 2%. Hence, central banks have held to current policies. (An exception was the Bank of Canada this month.) The result has been further asset price appreciation and more leverage. This combination will have to be adjusted, but not today. Nevertheless, markets are still hyper-sensitive to monetary policy musings.

High valuations and leverage make for a more difficult environment when there is a more market uncertainty concerning geopolitical shocks. As noted in a recent post, (AllianzGI Risk Monitor survey – Geopolitical risk on the rise, requires special thinking), geopolitical risks is on the rise as the top risk with investors. These types of risks are especially difficult to hedge given the impact across many asset classes. Growth expectations can be reversed quickly on a negative geopolitical event and leverage will make economies more sensitive to any shock. Investors have to think about strategies that will be more nimble to a negative geopolitical shock.

Related Posts

Iran, Venezuela, and the New Global Oil Order

Recent events remind us that balance in energy markets can be delicate. A conflict in the Middle East and the removal of a sitting President in Venezuela resulted in sharp moves across the energy industry in early 2026. Currently, the Iran War is creating havoc in crude shipments, affecting the world. While trouble in that […]

Decoding Metals Price Action

Markets often communicate more clearly through price action than through headlines. The dramatic surge in metals contracts is sending a powerful signal, but what exactly is it telling us? Traders frequently monitor inter-market relationships for early warnings. When one asset class moves unusually, it can ripple across the system or reveal deeper structural issues. In […]

2025 in Review: Markets, Policy, and the Path Forward

History never repeats itself, but it often rhymes. This is even more so the case this year, as Trump began his second term with similar but different disruptions to the markets. Rising stocks, normalizing inflation, and the AI boom took center stage. We discuss some of the key events below and try to anticipate where […]