“Enough with this diversification talk. I’ve got my 60/40, and I am happy!” The 60/40 stock/bond portfolio mix has become a standard reference or benchmark for many investors, yet its performance versus a truly diversified portfolio is mixed.

The Case for Diversification

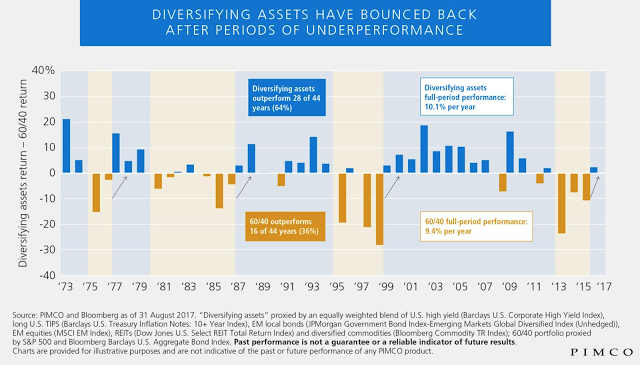

The diversified portfolio present above (high yield, TIPS, EM bonds, EM equities, REITs, and commodities equally weighted) is just one alternative diversifying mix of assets; nevertheless, the sample above shows that an equal-weighted portfolio will do better than a 60/40 stock/bond mix (S&P 500/Barclays Agg) about 2/3rds of the time. You could say that the positive opinion towards the 60/40 blend is a recency bias, with it outperforming a diversified basket in four of the last five years, not including the partial 2017 year.

Historical Context

The periods when there have been extended outperformance of the 60/40 blend relative to the diversified portfolio have been centered when there has been equity overvaluation in the US markets: mid-80s before the 1987 crash, late ’90s before the tech bubble, and the more recent period when US stocks have seen significant gains in asset inflation.

Strategies for Beating 60/40 in the Long Run

There are several ways to beat the simple 60/40 blend in the long run. One, add diversifying assets from the list used in the graph above. However, the excess return was based on the fully diversified portfolio versus the 60/40 blend. Two, add hedge fund strategies that have diversification of assets along with diversification of style. This, for example, could be a portfolio of managed futures programs that are already globally diversified across a broad set of markets, including equities, bonds, rates, currencies, and commodities. Along with asset class diversification, investors get strategy diversification that often weighs long and short positions by trends. The advantage of managed futures is the opportunity for adding convexity or portfolio gamma.

The Return-to-Risk Combination

Combining a robust US stock market with diversification from bonds has made for a triumphant return-to-risk combination. Still, as we have seen, there are no guarantees that this combination will always do well. Further diversification will better manage risk and allow for higher returns, especially after periods of one-sided performance.

Related Posts

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

The Evolution of Trading from Systematic to AI

Is AI the next step in the evolution of trading? History proves new tools storm the markets, then high adoption erases their edge. What can futures trading history teach us about AI’s trajectory? The 1980s: Rise of Rules-Based Trading Building on simple regression models that aimed to identify patterns across sectors, the 1980s showed that […]