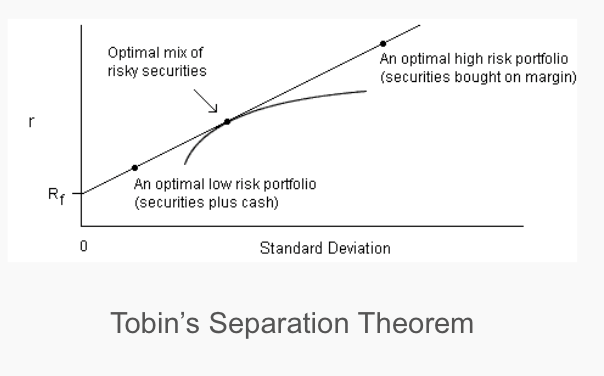

One of the greater principles of investment finance is Tobin’s separation theorem which is a powerful simple tool that can be used for any investment portfolio, but is especially useful when thinking about managed futures and alternative risk premiums. (Robin Powell reminded me of Tobin’s contribution in his essay, Can you really stomach the risk you’re taking?) There is a tremendous amount of useful investment advice through just applying the simplest of concepts.

Tobin’s Separation Theorem is elegant in its simplicity. Find the risky portfolio that maximizes the return to risk and then form a new portfolio that combines this risky portfolio with cash or leverage to find the level of risk that will make you comfortable. The new portfolio, set to the volatility you want, will be on the tangent line for the max return to risk. The new portfolio will be a combination of the risky portfolio and cash if you want less volatility. Similarly, the risky portfolio can be levered to a higher level of volatility.

The Tobin Separation theorem is especially useful for thinking about managed futures portfolios or alternative risk premiums using total return swaps. Because both use margin at a low level, the risky portfolio can be set at any level desired by the investors through notional funding.

For example, in managed futures, if the manager sets his base portfolio at a volatility target of 10%, the investor could fund a separate account for say $10 mm and set the notional exposure at twice the cash level or $20mm of notional exposure for 20% volatility on the $10 mm investment. The investor achieves the higher risk at the same return to risk trade-off. Managed futures managers understand the separation concept very well through their setting of volatility for their funds.

In the case of alternative risk premiums (ARPs), there may be a set of strategies that generate an information ratio of 2 but only has volatility of 2% and a return of 4%; however, a pension fund may have a discount rate of 7%. The ARPs may be a great investment but at a return of 4%, it will be significantly less than the expected return needed for the pension. The ARPs better be good diversifiers or there will be a return shortfall. In this case, the separation theorem tells us that we can view this as the risky portfolio that can be levered to a higher volatility that will be closer to the discount rate. Low volatility combinations of risk premiums can be levered through notional funding to a risk level more consistent with the desire of the investor.

Similarly, if an investor starts with a portfolio that has a beta of one but would like lower market exposure, it is easy to just reduce the beta exposure with an increase in cash to the level desired. It can be done through cash and the risky asset without resorting to greater complexity.

Find the best return to risk portfolio and then adjust to the volatility desired. If this can be done with investments which do not need to borrow such as swaps and futures, all the better. This approach is both elegant and simple.