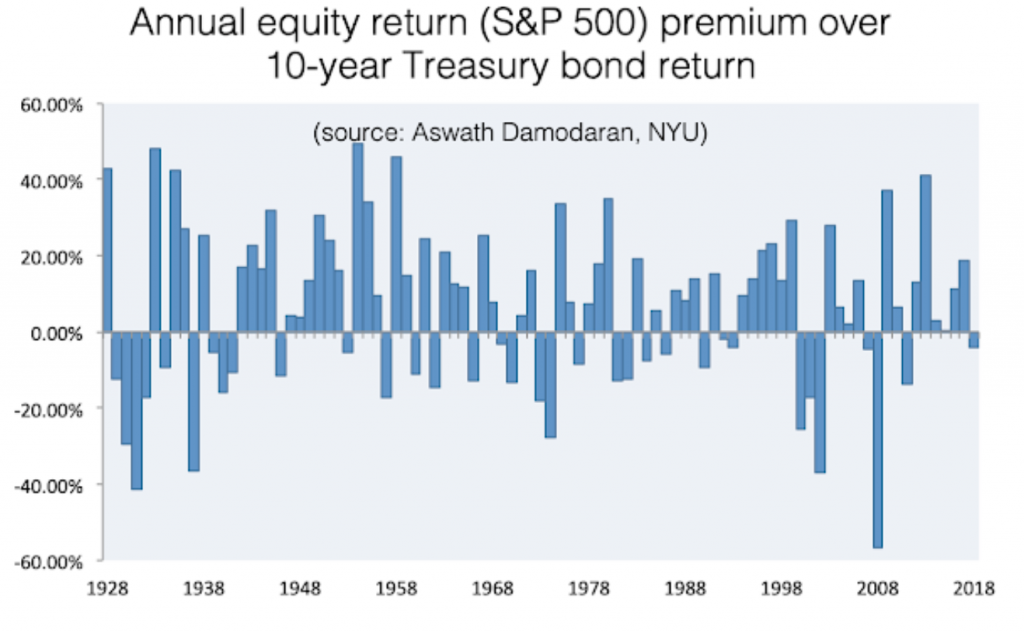

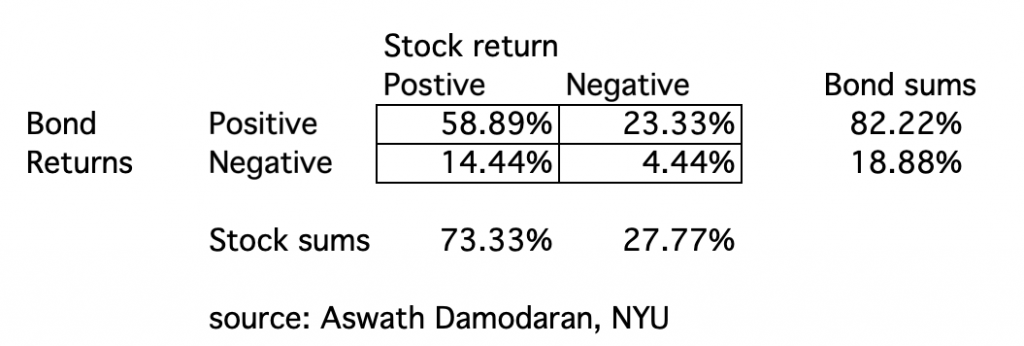

Many investors don’t appreciate that 2018 was highly abnormal for asset allocation. First, the annual excess return from holding equities is generally positive with the exception during recessions. 2018 was not a recession year. Yes, there was a slowdown in the fourth quarter, and growth expectations have slowed but the numbers do not suggest a recession at this point. Second, the likelihood that both stocks and bonds will be negative in a given year is very unusual. There has only been a 4.44% chance of this occurring over the last 90 years using the SPX and 10-year Treasury returns. It is highly unlikely that we will see a similar year in 2019. There have only been seven periods when the equity premium was negative for two or more years in a row.

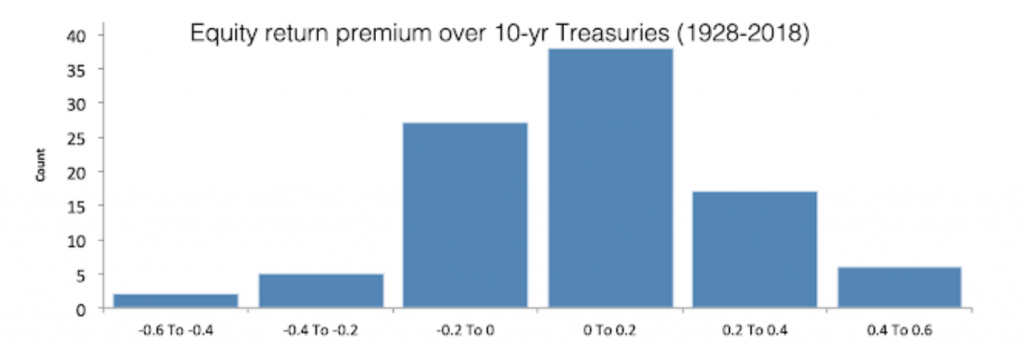

Additionally, the equity return premium over bonds is usually large. The arithmetic average is about 6.25 percent with a standard error of 2.25 percent.

Any bias should be to still hold strong equity risk exposure although a bias away from a 60/40 base case is warranted given the slower economic growth, uncertainty about liquidity, and higher volatility. The historical numbers always justify holding equities unless there is an exceptionally poor macro environment.