If there is an adverse market move and you want to change portfolio allocations and sell some securities, will you get a fair price? Any downside situations that investors will face will face a liquidity shortage. This is different than thinking about illiquid investments, where the knowledge concerning illiquidity is known.

The IMF Global Financial Stability Report of April 2019

More critical is the vanishing of liquidity for instruments that are usually liquid. Every investor should be prepared for a liquidity surprise. Like entering a theatre, the critical risk manager knows where the exits are. This issue is antiseptically discussed in the Global Financial Stability Report of the IMF for April 2019 as a “Special Report: Liquidity in Capital Markets.” It is a problem, but the report does not sound an alarm bell.

Two issues with market liquidity

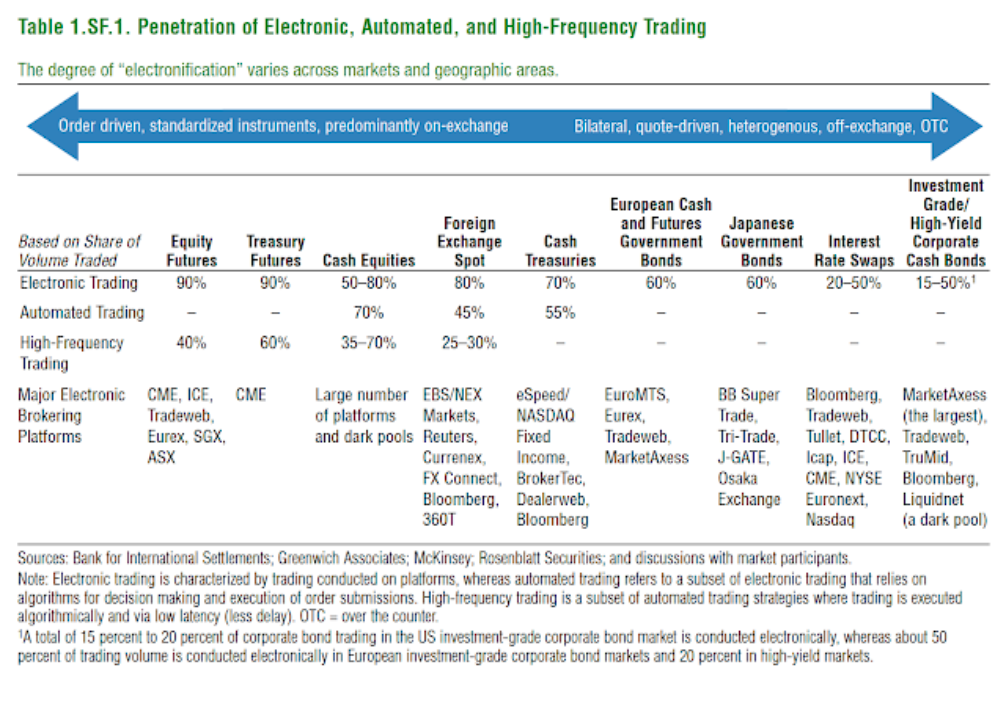

Two issues jump out when thinking about market liquidity. One, the liquidity market structure has changed radically since the Financial Crisis. It cannot serve all investors wanting to sell in a crisis. High frequency and electronic trading make the liquidity in a crisis more fragile, and the spread of technology is unequal. The trading future has come sooner for some. Two, the concept of market liquidity is fluid. Some asset classes are more liquid than others, and market liquidity last year was not the same as this year.

The dynamic nature of market liquidity

Market liquidity is dynamic. By some measures and for some markets, liquidity could be better than a decade ago, but there are some clear hot spots. For example, traders break up orders to reduce the price impact of trades, and high-frequency market-makers can make tight bid-ask spreads, but a shock can cause this liquidity to disappear quickly.

Related Posts

The 6 Biggest Myths About Diversification and Non-Correlation

“If everything in your portfolio goes up and down at the same time, you have a bad portfolio.” This simple but powerful observation from Mark Rzepczynski, former CEO of John W. Henry & Company, is one I think of often – for both my customers and my own investing. A losing position in your portfolio […]

Auto Loans: The Overlooked Credit Canary

Identifying weakness in markets can be a difficult task. Metrics like gross domestic product (GDP), equity market gains, and unemployment paint in broad strokes. Lenders often try to identify risk at a granular level. This might include tracking payments arriving late, higher credit card balances, increases in line of credit usage, or non-payment of insurance […]

Futures Margin Calls, Explained: Initial vs. Maintenance

A margin call is one of the phrases that scares a new futures investor the most. Often, they picture life savings getting wiped out in seconds, as it does in movies. The truth is not nearly as intimidating. Margin is simply a tool. One that educated investors often love. After all, if you expected your […]