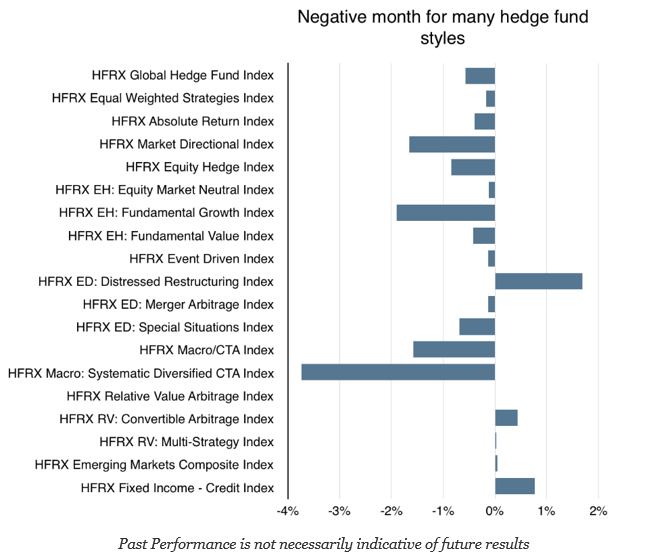

Hedge fund returns are a combination of alpha and beta risk exposure. The betas across different hedge fund styles are variable and dynamic. In general, beta will be below one, with most hedge funds showing market betas between .3 and .6. Some hedge fund styles, like managed futures, may be lower. Alpha can also be highly variable; however, we can say that in strong up markets, hedge funds are likely to underperform the market return. Similarly, it is not clear in strong down markets that hedge funds will generate a positive return in down markets.

With SPX, as the market portfolio, down 1.73% and the small-cap index (IWM) down over 4 percent, hedge fund returns this month were relatively attractive. At a .5 beta and a mix between large and small cap, equity-focused hedge funds should be down around 2 percent minus any alpha. Those strategies like special situations, mergers, and distressed, which may have lower beta and higher alpha, performed better. Those styles that are directional or may have a higher risk, given a focus on growth, should have done worse. In October, the strong decline in systematic and global macro managers was surprising. These styles should have done better in a down market.

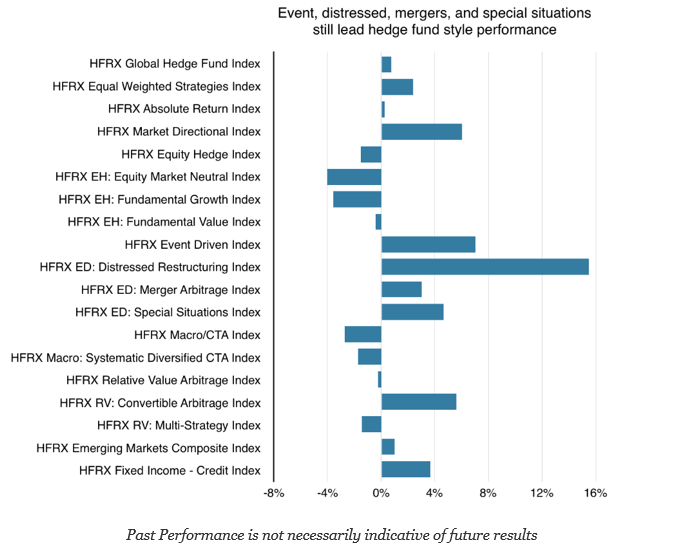

The year-to-date numbers are mixed, with only 5 out of 19 HFR hedge fund style indices generating returns over 4%. Eight styles have negative returns through October. On the other hand, small-cap stocks were up double-digit, and the S&P 500 index was up over 7% over the same period. Generalization should not be made, but holding passive portfolios has proved to be a better absolute return strategy this year.

A beta-adjusted (lower risk) strategy of stocks and bonds would have done better than many hedge fund styles in 2016. This difference has been increasingly the challenge put on hedge funds. Can hedge funds do better than a similar beta stock-bond mix? Put differently, can hedge funds generate consistent alpha? The answer seems to be yes for some selected styles but no for most.

Related Posts

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

The Evolution of Trading from Systematic to AI

Is AI the next step in the evolution of trading? History proves new tools storm the markets, then high adoption erases their edge. What can futures trading history teach us about AI’s trajectory? The 1980s: Rise of Rules-Based Trading Building on simple regression models that aimed to identify patterns across sectors, the 1980s showed that […]