Most stocks do not do well over their lifetime. If you randomly pick a stock or set of stocks there is a high likelihood you will not do better than T-bills and you will likely not survive for a long time. This should be well-known, but a new research paper really present some stark conclusions. This is a paper that is insightful and sobering for most investors. See “Do stocks Outperform Treasury Bills” by Hendrik Bessembinder.

While the conclusions are based on the well-used CRSP database, this work has not be done before or has not been highlighted in basic discussions on stocks. It is sobering because it tells you how difficult it is to make money by holding a stock portfolio. There are few papers that you will read this year that will change your view of stock investing as much as this fundamentally simple work. What is most important is that this research should change your priors on what are the risks from holding stock and simple fact that buying stocks can be a lottery ticket of poor returns coupled with a few out-sized skewed winners.

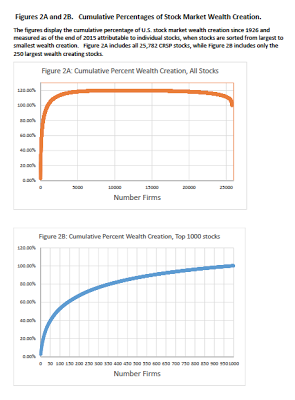

A cross-sectional review of stock performance shows that the distribution of returns is positively skewed, but 58% of all stocks will underperform 1-month T-bills over their lifetime and only about 4% of all stocks, the best performers, will account for all of the gains in the market. A key driver is that most stocks do not last a long-time, on average, seven years. There is a lot of risk when compounded equity returns are not normal, but the power of compounding is critical for generating long-term wealth.

These performance dynamics are all driven by the mechanics of skew. Compounding returns generates positive skew and the traditional focus on mean and variance masks the impact of differences between the mean and median returns for stocks. Most stocks will be losers in any month and across their lifetime. Only a few will be significant creators of wealth. If an investor is not fully diversified, he may come up a loser because he is just not holding the few winning lottery tickets in equity markets.

One could argue that holding passive indices is critical because you just don’t know who will be the few positively skewed winners. Alternatively, the active managers will say that this research suggests that insight is needed to look for these few winners. I will leave this discuss to others, but the critical issue is that risks may be larger that what many have imagined and that premiums are necessary given the risks faced.