Investors have shifted their focus to alternative risk premiums as a method for defining and allocating risk within a portfolio. The alternative risk premium framework can be employed in all asset classes but is especially useful in commodities given the large dispersion in markets and structural features that lend themselves to time varying risk premiums.

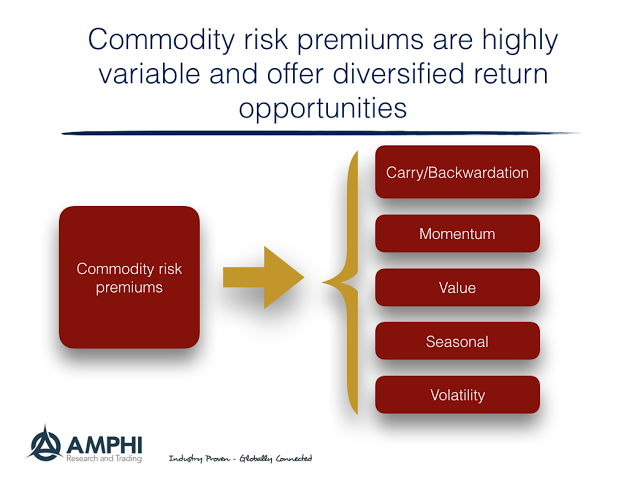

The general framework for alternative risk premium can be divided into a number of categories:

Carry/Term/Backwardation – (Backwardation/Contango) – There is more variation in backwardation across commodities and through time than what can be found in other markets given the sensitivity to inventory changes, supply shocks, and hedging pressure. The changing supply dynamics and demand for hedging creates a greater number of “carry” opportunities.

Momentum – (Time series/Cross-sectional) – Given the inelastic demand and supply for many commodities, there is likely to be greater price responses to any shock. The use of futures as a hedging tool means that many trades are not done for profit maximization but risk considerations. This creates trend and momentum opportunities.

Value – (Long-term price levels) – More so than other markets, long-term price can be serve as a value indicator. As often commented by market pundits, the solution to high (low) commodity prices are high (low) prices. Extended periods of low prices will lead to supply reductions which will serve as the mechanism for future price gains. Extend periods of high prices will lead to new supply and future price declines.

Seasonal – (Market situational) – More so than other asset classes, there are distinct seasonal patterns that lend themselves to changing risk premium.

Volatility – The volatility risk premium is present like other asset classes; however, these premiums are more diversified relative to other asset classes given the low correlation across commodity markets.

Commodity markets offer a wide set of alternative risk premium opportunities. These opportunities have improved with the end of the long-term super-cycle downturn. The dominate cycle factor has ended and has allowed more balanced investment opportunities.