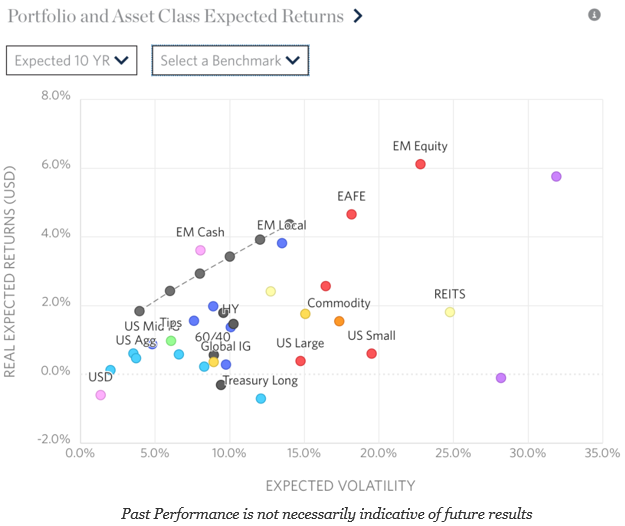

Strategic asset allocation as the name implies requires long-term return assumptions. There are often wide variations in the future forecasts. Many forecasts we have surveyed show positive expected returns, but the numbers are significantly lower than what investors have seen historically since the Financial Crisis. In general, Research Affiliates provides a good tool for analyzing the past and expected returns that we find helpful.

Fixed income annualized returns are still expected to be positive albeit closer to zero. Equities are expected to be, in many cases, half of what has been seen over the last five years. This does not seem unusual given the recent equity performance that is viewed as being in a bubble, but it is sobering to realize that overall returns for any allocation will likely be much lower. Pension will not be able to hit their return targets.

Similarly, there is a general increase in volatility over the next ten years as risk mean-reverts from their extreme lows. Many investors may feel destined to underperform performance target with higher risk if they follow these numbers.

So what can an investor do to break-out of this low returning asset class world? The best way may to change the rules of the game by asset allocating across strategies or risk premium and not asset class. This will not guarantee higher returns, but it changes the framework and enhances the set of possibilities.

Allocations to hedge funds may be the easiest way to enhance the choice set. One the one hand, lower asset returns will reduce the beta opportunities for hedge funds, but an increase in volatility will increase the dispersion of returns and opportunities which will allow for potential alpha generation. There are a host of reasons for alpha opportunities, but in general, more dispersion means greater opportunity for dislocations regardless of the expected factor returns. Given that hedge funds may be better able to control volatility, any optimization will tilt away from asset class market betas. The name of the game may be to focus on strategies not asset classes.