“Crisis alpha” is used as a quick description of managed futures trend-following, but there has been very little work to explain what the term means. A generic definition is that a crisis is when equity markets have a significant decline, but that definition tells us nothing about what will be the conditions for a crisis or when a crisis will occur.

It is a frustration for investors when this term is used. We only know by this definition that, ex post, if equities go down a lot, trend-followers are supposed to do well. That is not a basis for explaining when or why trend-following will do well. Wait until you lose 20% of your equity principal and then you will be happy with your managed futures exposure. While it is true, it is hardly an effective sales pitch.

We want to examine the idea of crisis alpha a little more closely. This is a topic for ongoing research. A crisis should be defined by some set of economic factors that represent stress in the macroeconomy. The stress or crisis will impact the pricing of financial assets and lead to price divergences. These divergences offer opportunities for trend-followers who profit long and short from price trend dislocations. By following variables that represent stress, we should expect above average trend-following returns.

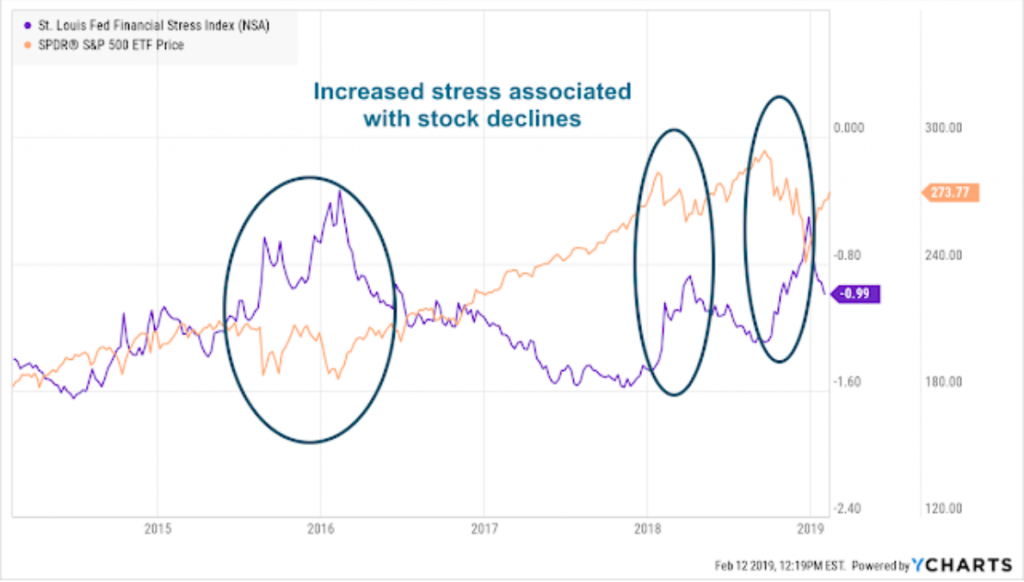

Trends is stress tell us something about trends in prices. Periods of financial stress are associated with price dislocations and these are the times that are likely to be profitable as markets reprice across the broad set of asset classes. Stress represents “bad times” and this is when prices fall to provide a premia for holding risk assets. Increases in stress are associated with declines in demand for risky assets.

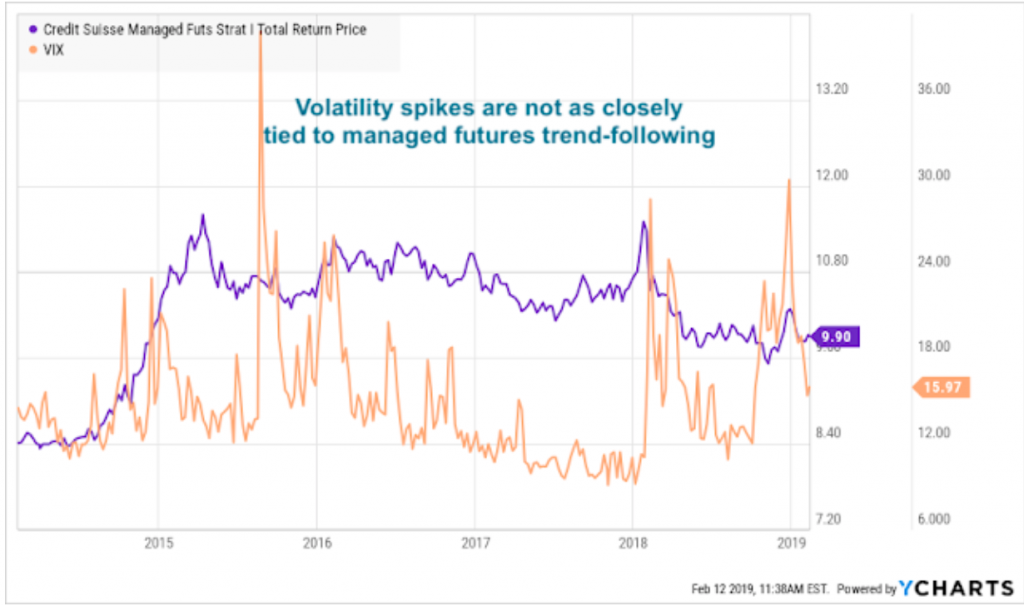

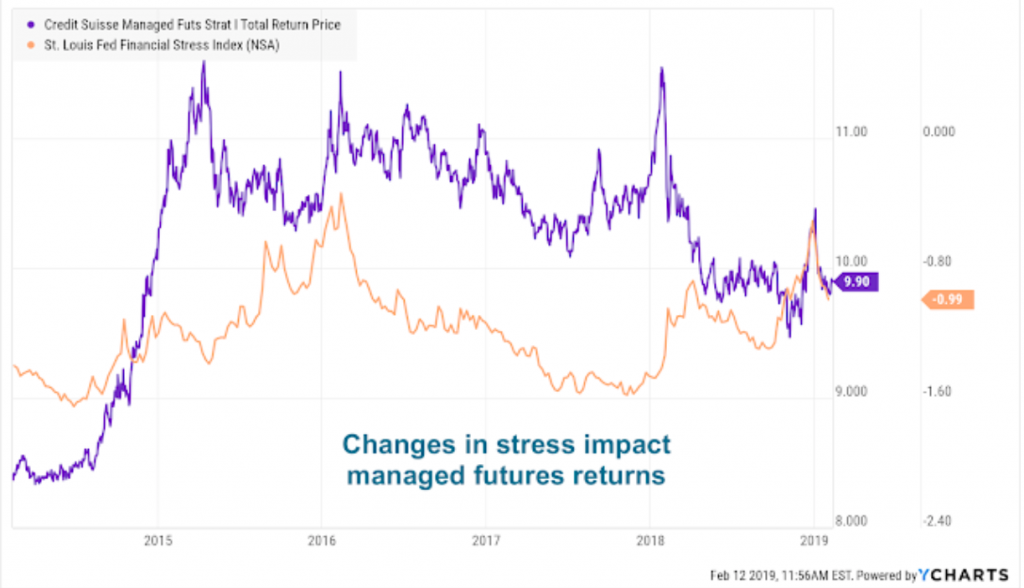

While there is a connection between equity returns and spikes in volatility, the link between volatility and managed futures is less clear. However, overall financial stress may be a better measure of when returns will be above normal. Financial stress includes volatility but is a broader concept that looks at a wider range of indicators.

Financial stress will change the risk preference of investors and force adjustment of portfolio exposures. The simplest investment response would be an adjustment from risk-on to risk-off behavior which will manifest in equity, fixed income, rates, currencies, and commodities. The broad repricing of risk increases the set of trend opportunities and returns in a manner that would not occur if there is a localized price disruption to a single market. Significant repricing allows for significant trend trading returns.

The times of maximum opportunity for trend-followers may be during times of increased market stress. Some may call this alpha but more likely it is just related to the lower beta or dynamic adjustment of beta. Remember the market risk premia is compensation for risk during “bad times” There is no risk premia if an asset actually does well during bad times because it exploits price dislocations by adjusting risk exposures or selling short. The low beta means trend-following does not receive a risk premia during normal times but positive returns during times of abnormal stress.

Look for periods of stress and investors will find better trend-following returns. No stress, like the post Great Financial Crisis period, and there will be limited return opportunities. Increased stress in the 2018’s fourth quarter generated returns for many trend-followers in December. The reversal of stress showed a reversal in trends and loses in January.