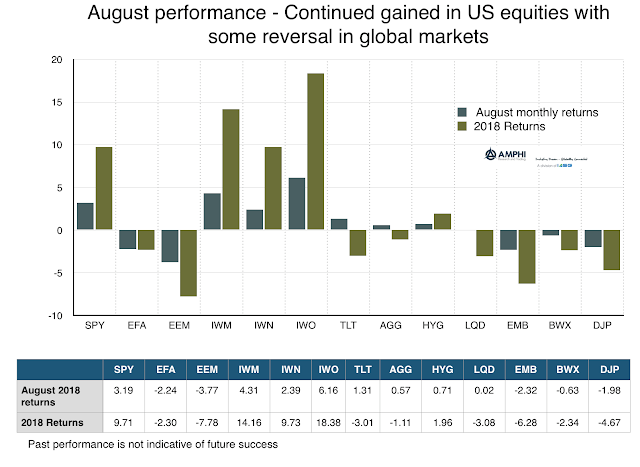

What can be called the twin disconnects of 2018 have continued this summer. There is the disconnect between market and political behavior. If you read the newspaper headlines, you would think there is government confidence crisis in the US, yet if you plot market activity, any investor would suggest the economy is in great shape. There is also the disconnect between US market activity and global market behavior. 2018 is shaping up to be a great year especially for small cap and growth benchmarks that are both up double digits with August again showing strong performance. Global and emerging markets, both equities and bonds, are sickly.

Disconnect of this magnitude do not last and as we come back from summer vacation and focus on asset allocation, the big issue is to either maintain or fade the major dislocations. Cut US stock exposure and add international equities. Cut risky equities and add to bond exposure. Unfortunately, it will take some major fortitude to make the switch against momentum, current macro data, and firm-specific strength. There is a wall of worry concerning high credit exposure and leverage, but it may still be early to make expensive allocation changes. Still, early after a great 8 months may be a safe strategy.

After hundreds of discussions with hedge fund managers, I am still surprised that there is a fear of revealing investment processes under the assumption that someone will steal their ideas and intellectual capital. There are few investment styles that are truly unique and special. What is special is still strategy execution – the practical process of delivering returns. Skill is with the decision-making execution of information and strategy.

All hedge funds are not created equal as the return box chart shows for the post Financial Crisis period. There is a significant amount of dispersion across hedge fund styles. Over the period 2009-2018, the difference between the best and worst hedge fund category is almost 7 percent after we account for global equities and bonds.

The attraction to private equity and other less liquid alternatives is clear from the Guide to Alternatives by JP Morgan Asset Management. The return profile is much higher for private equity and debt funds than more liquid alternatives and global bonds; however, the dispersion in returns is multiples higher than what can be expected from other public categories.