Market Overview: Gasoline

- Current demand has climbed to a robust 9 million bpd which is 3.2% higher than the three year average

- At 9.84 million barrels per day, soaring U.S. gasoline production is a whopping 10.6% higher than the three year average

- As of this report, the NYMEX spot gasoline price is at $2.99/gal which is 7.6% below the three year average

- According to the EIA, this summer’s monthly average retail gasoline price is expected to peak at $3.66 per gallon in May and then decline to $3.46 in September. The current average price is $3.596 per gallon.

Outlook

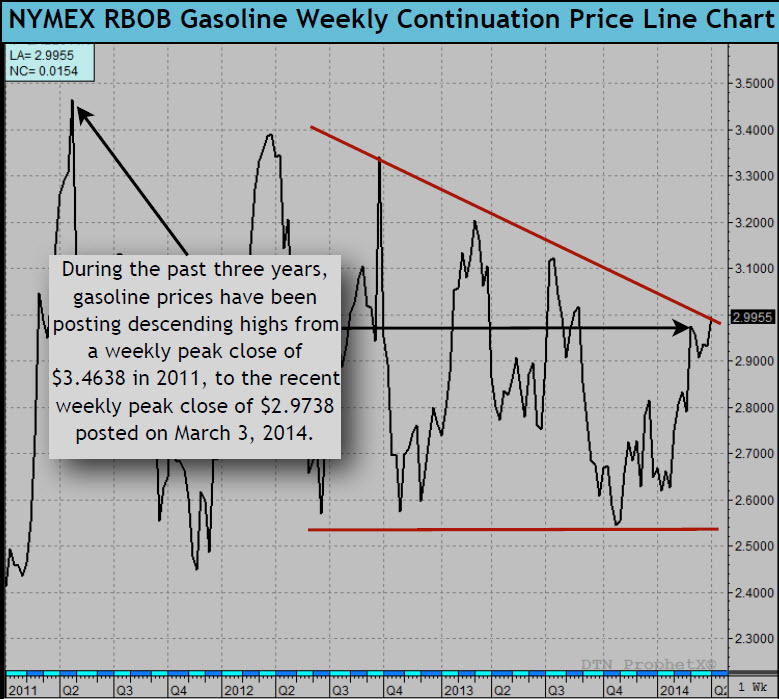

During the past three years, gasoline prices have been posting descending highs, from a peak of $3.47 in the second quarter of 2011 to the recent peak price of $3.05 posted on March 3, 2014. We think gasoline prices will have limited upside due to two main factors:

- Brent crude oil comprises about two-thirds of the price of northeast (NYMEX) gasoline. This summer, we expect Brent crude prices to average $105 or $2 below last summer’s levels.

- Soaring gasoline production will be more than enough to meet summer driving demand and keep prices in check. Given the above-mentioned factors, we think summer NYMEX gasoline prices will remain rangebound between $2.65 and $3.10 per gallon.

Summary

Soaring domestic shale oil production and increased refining capacity have brought a measure of supply/demand balance to the oil complex. As a result, market volatility and price compression has become more pronounced. From a trading perspective, we are adjusting our directional trading strategies to fit the current market environment by reducing individual trade strategy profit goals as well as the concomitant risk. In addition, we will from time to time, utilize option strangles and credit spreads to bracket the market when conditions warrant. Up until last year, bracketing strategies comprised approximately 25% of our trading activity and we are very adept at managing the risk associated with these structures. On a final note, we will be bringing WTI crude oil trading back into the trading portfolio as we now believe the current market better reflects the underlying fundamentals of supply and demand, and less influenced by the trading activity in the WTI/Brent spread. Please feel free to review our performance overview.

Related Posts

Bowmoor Capital – A Different Approach to Trend Following

Competing head-to-head to outsmart others doing the same strategy is often a tough road. In trend following circles, giants like Man AHL, Winton, and Aspect dominate assets under management. This enables them to hire top PhDs, deploy better technology, test ideas rapidly, and outspend smaller players on sales and marketing. So how can a smaller […]

Cayler Capital | April Performance Commentary

After finishing off one of the wildest quarters of my trading career, April managed to take the cake. For those that missed it (not sure how you possibly could have), oil settled negative $37. The effects of this were immediate: risk barometers had to be recalculated, option models switched, and most importantly was the immediate […]

AG Capital: Fade to Famous

There’s something about being quoted in the Wall Street Journal or making it onto Bloomberg TV that often leads to terribly inaccurate judgement calls (at least in the short-term). A classic example of this is Ray Dalio’s famous interview from Davos in early 2018, where he declared that “If you’re holding cash, you’re going to feel pretty stupid” just before the market cratered -12% and potentially may have begun a topping process for the entire bull market run from 2009.