Investment consultants are a force to the reckoned with in the pension world. They advise and drive many pension decisions around the globe. Consultants literally control trillions of dollars of allocations to managers through their recommendations, yet there have been no studies on the effectiveness of their choices. There may be limited argument that they provide useful information and education for pension managers, but they also give specific advise on managers, so an analysis of their picks is extremely valuable. The result may surprise you. Their investment manager picks do not outperform some simple benchmarks.

The recently published study in the Journal of Finance, “Picking Winners? Investment Consultants’ Recommendations of Fund Managers” [PDF], makes a carefully researched assertion that consultant recommendations have little value. Worthless may be too strong, but that is close to what most would conclude when they read the paper. Given all of the work on trader skill and market efficiency, this should not be surprising. But, given that consultants supply their work do leading pensions, it is should be surprising that no one has called them on their recommendations.

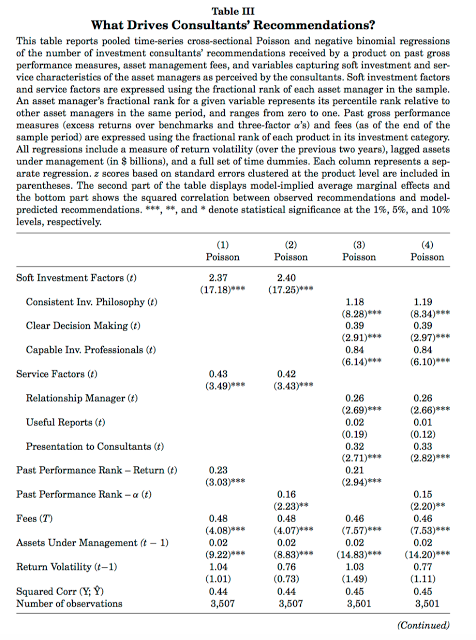

The authors do a very careful job of researching this topic through analyzing what drives recommendations. Recommendations are driven by more than past performance but by soft factors such as philosophy, service, fees, and size. Consultants are not return chasers but are slaves to size which is a key driver for this results. The soft factors also seem to be key drivers for recommendations. The due diligence process identifies managers that have a well-defined process and can explain well. Given their client base and job, consultants have to be size sensitive. Perhaps in an imperfect world, the best they can do is conduct due diligence and make the best recommendations given size constraints.

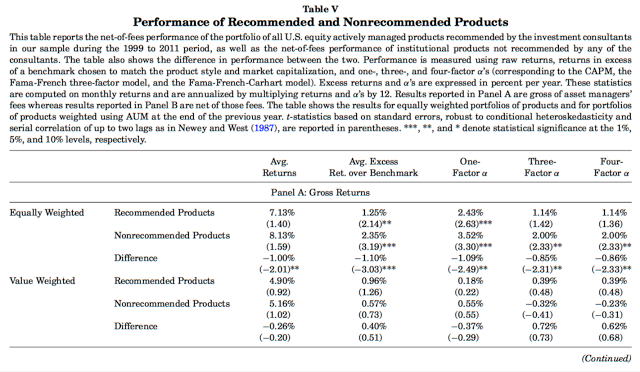

Nevertheless, it may be too easy to let them off the hook based on the size argument. First, there is no evidence of outperformance and equal weighted portfolios of recommendations underperform. Second, these performance results hold for a number of different factor models. Third, the size or scale effect can explain the underperformance, but it cannot explain why the recommendations do not outperform alternatives.

Use your consultants carefully. If you want them to sift through managers and find those that meet size criteria and have well-defined processes, you are in safe ground. If you are asking them to pick future winners, beware. The responsibility of picking winners can be delegated but don’t expect that they will be able to find a holy grail of outperformance. It seems like sticking to basics is still best. Stay diversified with asset classes and strategies. Don’t try and select individual winners, but focus on the right asset allocation and adapt your betas to the environment when necessary.