A recently published Fidelity Global Institutional Investor survey suggests that more asset allocation changes will be made in the next one to two years than shown in their last two surveys in 2012 and 2014. This survey anticipates what we are all thinking – it is a new investment world with a Fed becoming more aggressive and the politics of populism sweeping many countries. The post-crisis investment world of boundless liquidity and asset performance catch-up has ended. We are entering a new period of two-way market views. There is more uncertainty on market direction so we are likely to see more divergences in asset allocation.

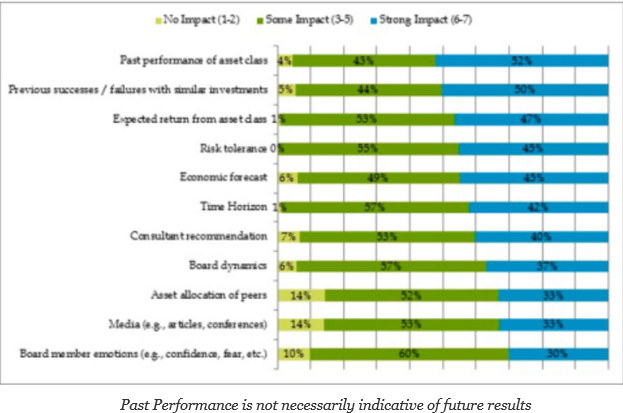

When asked about the top concerns for investing in their portfolios, the three top answers were all boar performance; what is past performance of an asset class, what is the expected return from an asset class, and where has there been success and failure with investments. Perhaps performance is always the top issue in the minds of managers, but the survey highlights particular focus during this period of transition.

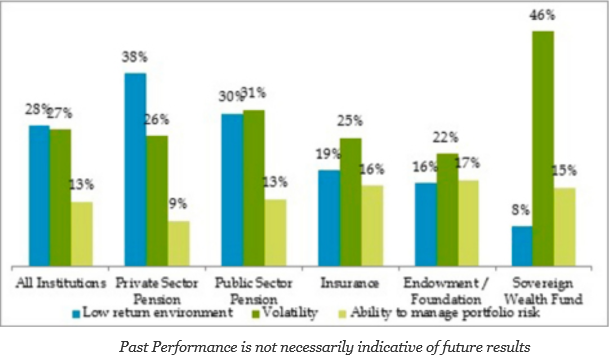

The survey also highlights the difference between endowments and pension funds. The pension funds have as their top focus the low volatility environment. For pensions, low returns create a funding gap that has to be made up through cash injections or in the case of states increases in taxes. For endowments and sovereign wealth funds, the focus is on volatility and ensuring smooth return streams and little downside risk. Given their differences, it should be expected that their asset allocations should not be the same. Pensions will focus on return and endowments will focus on diversification.

There are some additional nuggets in the survey that provide food for thought. Institutional investors are expecting a 6% return environment and 2% alpha every year. Both forecasts seem to be aggressive in this uncertain world. The real surprise is that 46% of European and Asian investors have changed their investment approach in the last three years. The number is 11% in the Americas. This is a radical change in portfolio thinking although it is not clear what it entails. Allocations may change within an approach but changes in basic approaches suggest that managers are unsatisfied with the methods for reaching their expected returns.