No investor wants to bear downside risk. Well, perhaps more precisely, no one wants to bear downside risk without extra return compensation. Strong asymmetric risk preferences create the reason for a volatility risk premium – the empirical fact that implied volatility is higher than realized volatility. What the volatility risk premium states is that if you buy an option you will pay more in terms of volatility than what the market will give you in actual volatility. In a very simple but elegant paper in the Journal of Alternative Investments called “Embracing Downside Risk”, some practitioners look at the compensation toward downside risk through a decomposition of returns by strategy.

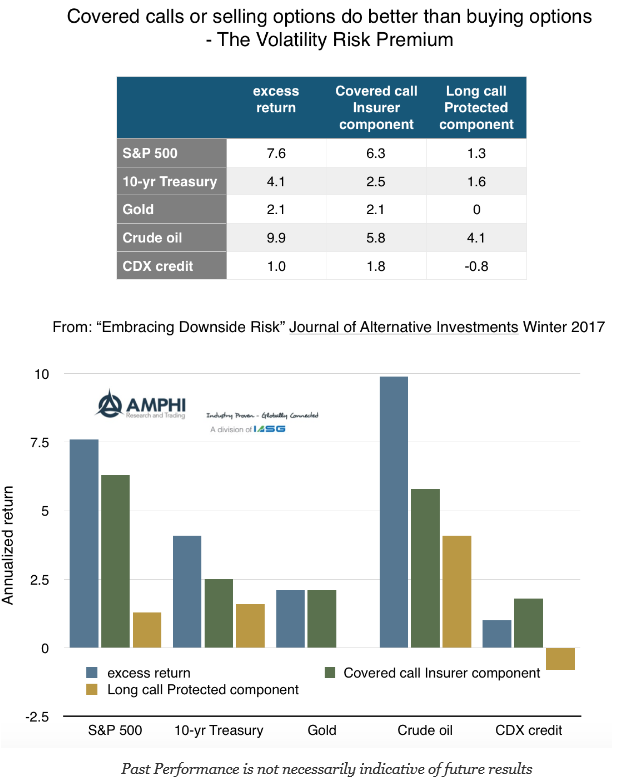

We know from parity conditions that the excess return for an asset can be broken up into two option strategies. For example, the returns for the S&P 500 index can be divided into a long call position and a covered call positions, or a short naked put and a long stock position with a protective put. The covered call or short naked put can be thought of as an insurer’s component and will represent the return received for taking on downside risk. Alternatively, the long call or cash plus put position is the protected component which reduces downside risk. It is the return for a protected position. The combination of the insured and protected components will equal the underlying cash return.

The authors find that in a set of cases across a number of assets classes over a long time horizon, the compensation for being an insurer is significantly higher than a protected position. The covered call or naked put excess return is not close to being the same as a protected position. The market prices downside risk greater than protected upside components. So maybe an investor should be willing to provide this insurance if you can avoid the really “bad times”? You are getting paid well to provide the insurance in the option markets.

We will say that market perception is that you should never take on this downside risk. If you go to your clearing firm and say you have a strategy that shorts naked puts or even follows a covered call strategy, risk manager will want to have a very serious talk to you about risk. Firms will also ask for more margin regardless of your reputation or the rates posted by exchanges. Good luck finding the firm to help you, yet the return data suggest that it may be a risk worth taking. Forgetting the numbers for a second, risk aversion is very strong even among risk experts. This tells me that there could be opportunity here by being an insurance writer.