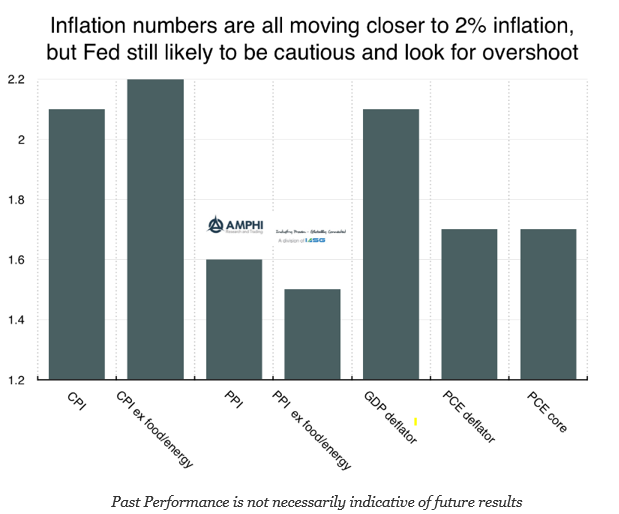

Current inflation numbers are all moving closer to 2%, but there is no special policy action from hitting or exceeding this rate. In fact, a cautious Fed is more likely with the most aggressive forecast being 2-3 rate moves. The Fed has not followed a mechanistic policy even though they have stated they are “data driven”. The most likely forecast will be to fade the earlier musings of the Fed.

It is notable that the PCE index which is the Fed preferred inflation index is still below 2%. The PPI which has a loose link with the CPI but may provide a noisy lead is also below the 2% target. It is the CPI which has moved above the target, yet policy-makers place less weight on its importance. Nominal wages are increasing by just under 4% but this change has fallen over the last year.

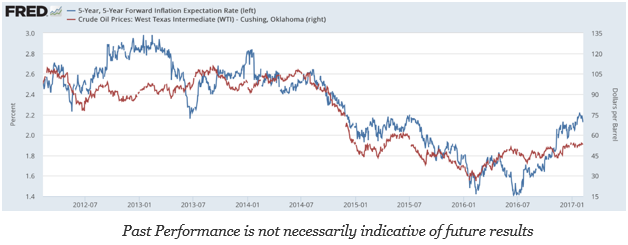

The latest 5-yr 5-yr forward inflation expectations may have temporarily topped, but the variation around this number suggests that this decline is noise at this time. These inflation expectations have moved closely with oil price levels. Expectations moved quickly higher with oil gains in 2016 and have topped with the range-bound behavior in oil.

Increases in inflation expectations may abate with delays in fiscal policy. A slowdown in US federal spending or a delay in a tax cut will likely push inflation and expectations lower. Asset allocation decisions based on higher inflation may not see immediate performance gains. There may be a chance for investors to wait and see how new policies unfold before responding to inflation.

Related Posts

2025 in Review: Markets, Policy, and the Path Forward

History never repeats itself, but it often rhymes. This is even more so the case this year, as Trump began his second term with similar but different disruptions to the markets. Rising stocks, normalizing inflation, and the AI boom took center stage. We discuss some of the key events below and try to anticipate where […]

The Bankruptcy Cycle Returns: Delayed Failures and the Cost of Easy Money

Proper forest management requires clearing dead brush, protecting high-risk areas, and conducting controlled burns. As January 2026 approaches, marking the one-year anniversary of the devastating Southern California wildfires that destroyed over 16,000 structures, we examine the mistakes made and how those lessons apply to the financial markets. Much like forest fires, risk can be mitigated […]

How Irrational Is It? Valuation Ratios and Bubble Risk

For anyone who has ever ridden a roller coaster, the distinct sound of the chain nearing the top of the first drop echoes in our ears. Click, click, (slower) click…. Anticipation builds right before we experience the massive first drop, picking up speed on the way down. If only the equity markets provided the same […]