One of the leading questions for any investors or asset allocator is what drives interest rates. If you know the factors that will cause rates to rise or fall, you have a significant edge in the market. Any decomposition of rates will fall into three broad categories, the real rate of interest, expected inflation, and a risk premium. What has been a puzzle for many researchers is that while there is an expectation that there should be a positive relationship between growth and interest rates based on inter-temporal smoothing, there has not been found a strong empirical relationship like what has been with expected inflation.

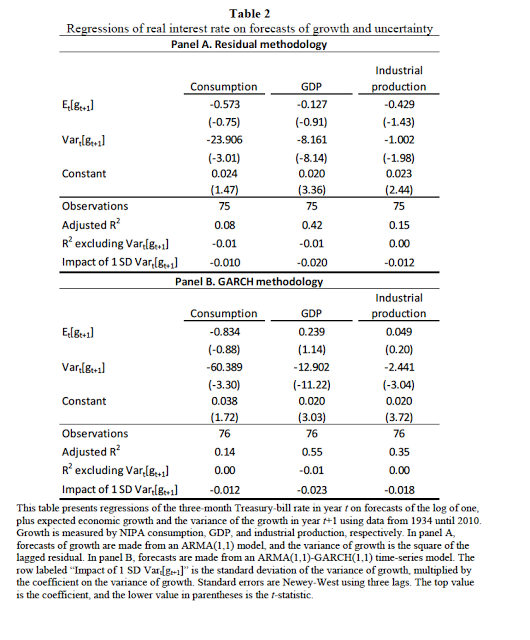

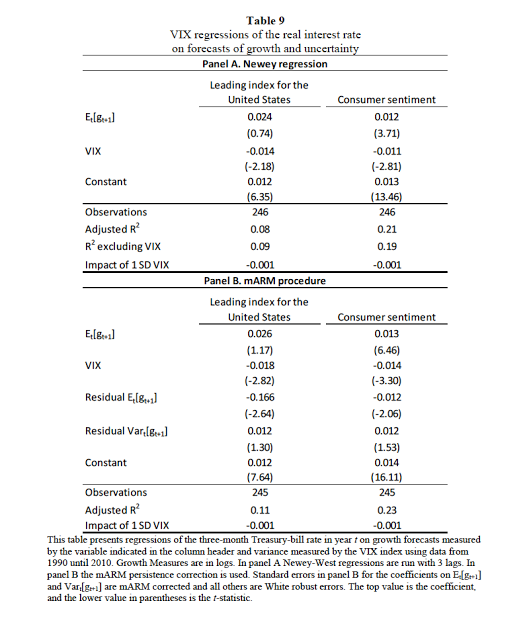

An alternative channel for driving rate moves is that a precautionary saving story can explain a negative relationship between real rates and macro economic uncertainty. A carefully researched paper by Samuel Hartzmark called “Economic Uncertainty and Interest Rates” finds a strong negative empirical relationship between rates and growth uncertainty. This statistical relationship is found not only in the US but also around global bond markets and through long historical periods. The relationship all exists through a number of measures of macroeconomic growth as well as the VIX measure of uncertainty.

What this research provides is a strong foundation for looking at uncertainty as a key driver of rates. If there is significant dispersion in expected economic growth, there will be a precautionary demand for short-term cash instruments. If uncertainty declines there will be less downward pressure on rates. The precautionary savings story suggests that rate changes may not tell us anything about growth but will suggest a link with demand for safety during periods of uncertainty.