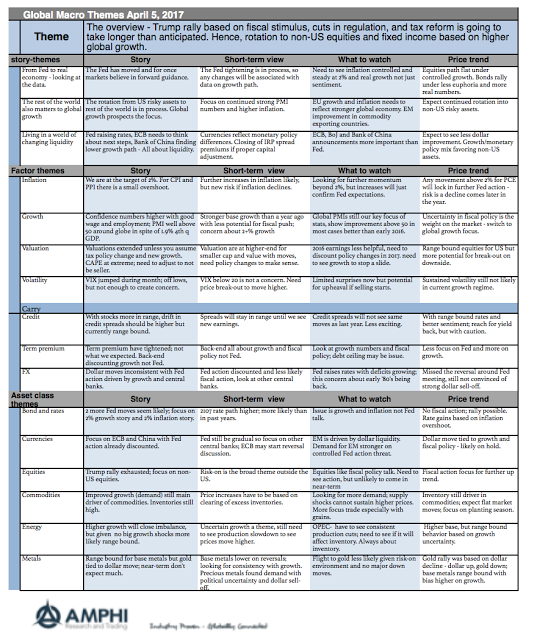

March was a tough month for making any economic judgments. The Trump rally in equities was expected to continue, but reality has been a switch to non-US risky assets. A bond sell-off was expected given Fed action combined with more fiscal policy revelations. It did not happen. The dollar was expected to continue its rally based on further confirmation of the Fed being out of step with other central banks. It did not happen.

In reality, stocks were ranged to the downside, bonds rallied albeit still in the range for the year, and the dollar sold-off on Fed action. Perhaps euphoria about fiscal policy change clouded the reality of current macroeconomics. We are neither in a strong secular stagnation or meaningful financial cycle adjustment, but the environment is still not ready for a new era of growth. Further upside in rates, the dollar, and equities will only come with a clear set of less uncertain policies and that is not likely this quarter.

The market focus has to be on the simple core of macro forecasting, real growth, inflation trends, capital flows, and central bank action. The emphasis has to be on what is and not what policies might be. Of course, forecasting is forward-looking, but given the level of uncertainty, the trends in economic data and actual prices are what should dominate and if the trends change, opinions have to be flexible and also change.

Related Posts

Iran, Venezuela, and the New Global Oil Order

Recent events remind us that balance in energy markets can be delicate. A conflict in the Middle East and the removal of a sitting President in Venezuela resulted in sharp moves across the energy industry in early 2026. Currently, the Iran War is creating havoc in crude shipments, affecting the world. While trouble in that […]

Decoding Metals Price Action

Markets often communicate more clearly through price action than through headlines. The dramatic surge in metals contracts is sending a powerful signal, but what exactly is it telling us? Traders frequently monitor inter-market relationships for early warnings. When one asset class moves unusually, it can ripple across the system or reveal deeper structural issues. In […]

2025 in Review: Markets, Policy, and the Path Forward

History never repeats itself, but it often rhymes. This is even more so the case this year, as Trump began his second term with similar but different disruptions to the markets. Rising stocks, normalizing inflation, and the AI boom took center stage. We discuss some of the key events below and try to anticipate where […]