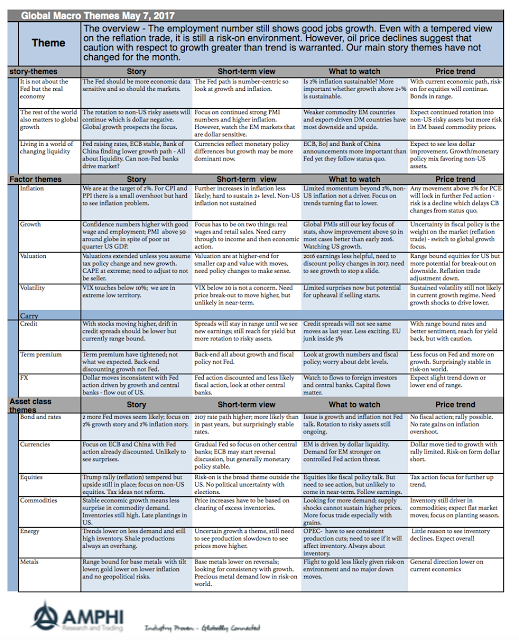

The Fed and other central banks are not that important in the current thinking of investors. The focus is not on the policy musings of bankers but the real economic data. All that matters is whether growth has a strong chance to be above trend and whether global DM inflation has a chance of reaching and sustaining 2%. We are skeptics of both occurring.

A strong growth trend will allow the current risk-on environment to continue. Inflation moving higher will reinforce more conservative or hawkish central banker views. The euphoria toward the reflation trade is coming back to reality and is likely to move more closely to the real data. Growth may be stronger than last year but break-out trends in growth are unlikely even with strong PMI’s signals. Bond investors have stayed cautious about this risk-on world and falling oil prices signal weaker demand.

There is a disconnect between equity and bond market views of the world. We do not intend to fight the risk-on sentiment and side with the more conservative bond view, but any risk-on overweight is modest in the current environment.

Related Posts

Iran, Venezuela, and the New Global Oil Order

Recent events remind us that balance in energy markets can be delicate. A conflict in the Middle East and the removal of a sitting President in Venezuela resulted in sharp moves across the energy industry in early 2026. Currently, the Iran War is creating havoc in crude shipments, affecting the world. While trouble in that […]

Decoding Metals Price Action

Markets often communicate more clearly through price action than through headlines. The dramatic surge in metals contracts is sending a powerful signal, but what exactly is it telling us? Traders frequently monitor inter-market relationships for early warnings. When one asset class moves unusually, it can ripple across the system or reveal deeper structural issues. In […]

2025 in Review: Markets, Policy, and the Path Forward

History never repeats itself, but it often rhymes. This is even more so the case this year, as Trump began his second term with similar but different disruptions to the markets. Rising stocks, normalizing inflation, and the AI boom took center stage. We discuss some of the key events below and try to anticipate where […]