It has been a tough period for making money in commodities especially if you have been a long-only index investor. When the super-cycle turns down, there is no place to hide even trading from the short-side has been challenging. Both momentum and carry-based approaches for finding opportunities have suffered during this period of prolonged decline; however, there may be hope for investors through using different portfolio weighing schemes when building commodity portfolios.

A recent paper which analyzes different approaches to weighing momentum and carry shows that there can be significant gains in return and information ratio relative to a commodity index and an equal weighted portfolio. See “How do portfolio weighting schemes affect commodity futures risk premia?”

We will show some of the results from this research, but first it is important to provide an intuitive feel for why different portfolio weighing schemes may work.

Fact 1: Volatility is high and variable and correlations across commodities are lower than what will be found in other asset classes. There is more benefit from weighing and adjusting to volatility than if correlations are high and volatility is stable.

Fact 2: Momentum seems to work in commodity markets, but performance will be affected by the changing volatility.

Fact 3: Backwardation and contango as a carry strategy is effective, but it can be swamped by large up or down price trends.

Conjecture: Using dynamic portfolio weighting schemes may have the ability to improve performance through adapting to changes in the covariance matrix.

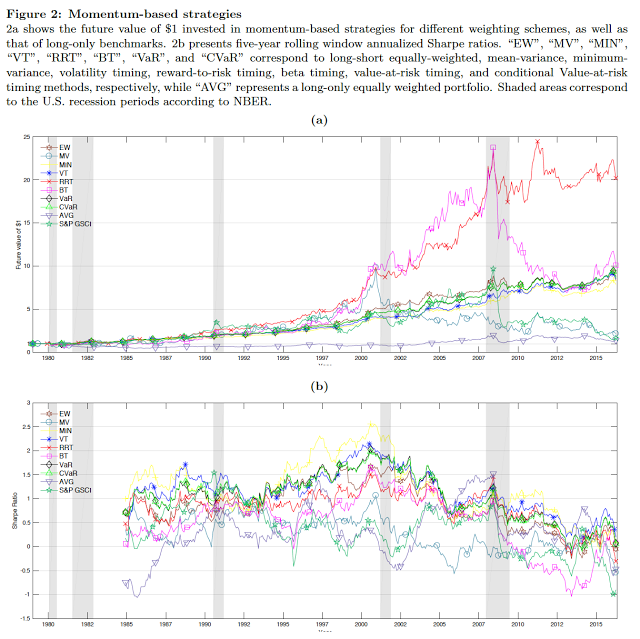

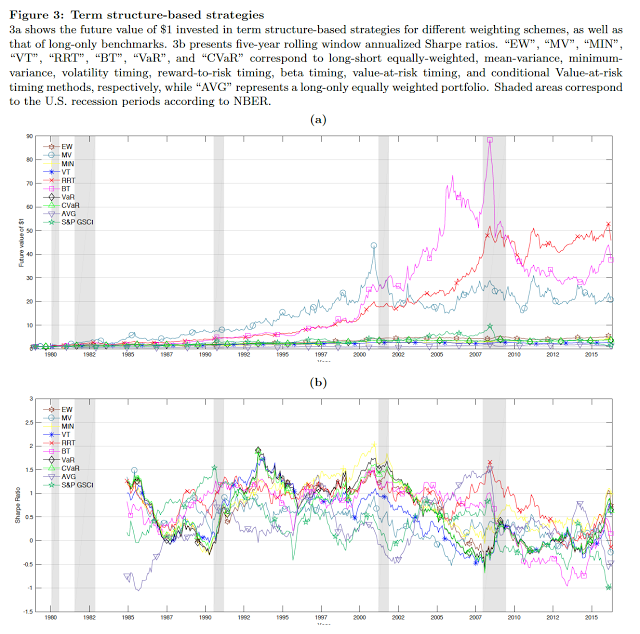

The researchers find that using different weighting scheme with momentum and the slope of the forward curve can add significant value. To help the process, they use a trick to form “backwardated” and “contangoed” portfolios for expected return based on the slope of the forward curve and momentum. This is done in order to have them behave like long-only constrained portfolios. This makes the portfolios less sensitive to return errors. Once the return engine is set, the researchers look at different weighing schemes based on volatility or timing criteria. Relative to an average and S&P GSCI benchmark, the researchers look at:

- equal weighted (EW)

- mean variance (MV)

- minimum variance (MIN)

- volatility timing (VT)

- reward to risk timing (RRT)

- beta timing (BT)

- VaR timing (VaR)

- CVaR timing (CVaR)

The performance profiles and Sharpe ratios show the clear impact of sizing the portfolio properly. The sizing matters even if you are using the same return generating engine.

Using different weighing schemes with carry and momentum will improve significantly performance relative to an index. Adjustments and rebalancing is done monthly without any risk management schemes. Be a timer or minimize portfolio risk, but don’t sit on the sidelines with passive commodity investments.

Related Posts

Iran, Venezuela, and the New Global Oil Order

Recent events remind us that balance in energy markets can be delicate. A conflict in the Middle East and the removal of a sitting President in Venezuela resulted in sharp moves across the energy industry in early 2026. Currently, the Iran War is creating havoc in crude shipments, affecting the world. While trouble in that […]

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Decoding Metals Price Action

Markets often communicate more clearly through price action than through headlines. The dramatic surge in metals contracts is sending a powerful signal, but what exactly is it telling us? Traders frequently monitor inter-market relationships for early warnings. When one asset class moves unusually, it can ripple across the system or reveal deeper structural issues. In […]