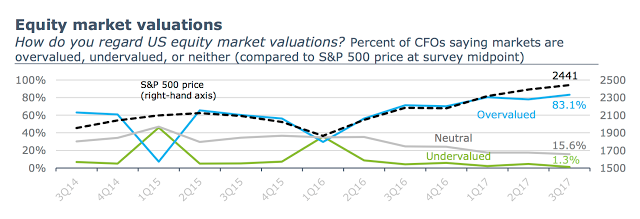

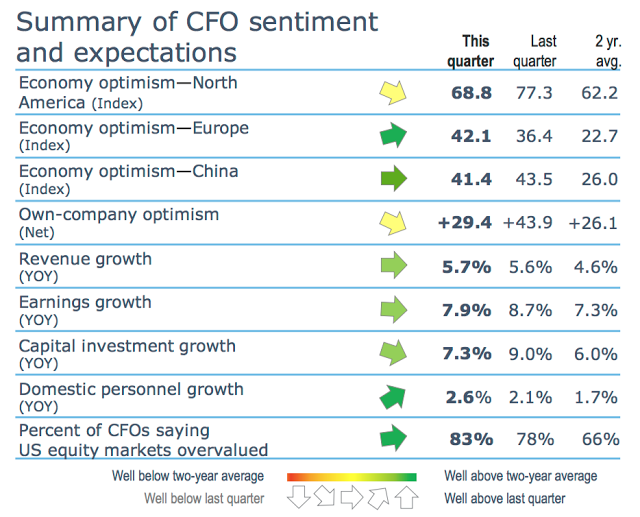

The Deloitte CFO quarterly survey should give any investor pause for concern. The numbers for this quarter show that 83 percent of those surveyed believe the equity market is overvalued. The number is at all time highs but has been around 80% all year, in spite of the market continuing to go up. Perhaps the CFO’s forecasts are wrong; however, I have more concern from the economic sentiment and expectations.

Economic optimism for North America is declining. Company specific optimism is also falling. Revenue and earning growth are moving sideways. The only real positive is European economic optimism and to a lesser extent domestic personnel growth. The combination of overvaluation and less optimism should make any market correction more likely.

As we begin the fourth quarter, the survey suggests that plans for more defensive asset allocations should be pushed forward with less delay. Now, the tax plan that many have been hoping for has shown some signs of life since the survey, but its complexity suggests that, at this time, it will not change the current CFO sentiment.

After hundreds of discussions with hedge fund managers, I am still surprised that there is a fear of revealing investment processes under the assumption that someone will steal their ideas and intellectual capital. There are few investment styles that are truly unique and special. What is special is still strategy execution – the practical process of delivering returns. Skill is with the decision-making execution of information and strategy.

All hedge funds are not created equal as the return box chart shows for the post Financial Crisis period. There is a significant amount of dispersion across hedge fund styles. Over the period 2009-2018, the difference between the best and worst hedge fund category is almost 7 percent after we account for global equities and bonds.

The attraction to private equity and other less liquid alternatives is clear from the Guide to Alternatives by JP Morgan Asset Management. The return profile is much higher for private equity and debt funds than more liquid alternatives and global bonds; however, the dispersion in returns is multiples higher than what can be expected from other public categories.