“You can’t predict but you can prepare.”-Howard Marks

A simple explanation for looking at a portfolio as a bundle of diversifiable risks is presented nicely in the new book, Rational Investing; The subtleties of asset management by Hugues Langlois and Jacques Lussier, two excellent researchers and money managers.

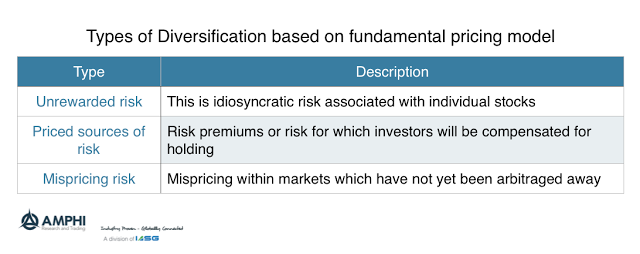

There are three types of risks that can be diversified: unrewarded risks which are the ones that can be diversified through holding a broad market basket, priced risks that are associated with risk premiums, and mispricing risks which have yet to be arbitraged away.

Most investors have a clear idea of what it means to diversify unrewarded risks; consequently, there is a strong current focus on alternative sources of risk and the risk from mispricing.

Mispricing risks can be taken advantage of over the short-run, but are unlikely to last and will diminish as more investors invest in these opportunities. Priced sources of risk are perhaps the most critical focus for portfolio managers because they represent both the best opportunities as well as hidden risks. These risk premiums can include growth, inflation, and liquidity as well as a host of other factors that may be time varying. Portfolios can be tilted to either take advantage or eliminate these sources of risk once they are identified. These risk premiums will often be time varying with the business cycle, credit cycle, and risk preferences.

For hedge fund investing, there is real value understanding the risk premiums or mispricings that the managers are trying to exploit. A true alpha producer is able to exploit mispricing, but for many, since these risks are fleeting, there may be a desire to have them diversified away. While time varying risk premium can be a source of return for money managers and hedge funds, the premium is compensation for specific risks and may not be attributed to manage skill.