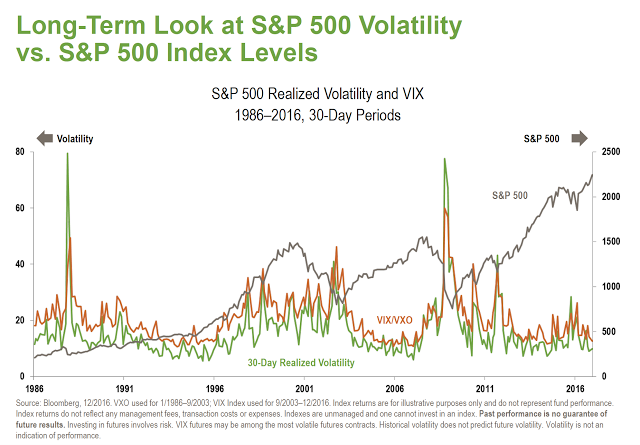

Investors should be concerned about the unintended behavior from low volatility. Low volatility will lead to higher volatility in the future when investors become complacent about risk, the “Volatility Paradox”. This paradox has been discussed by Richard Bookstaber as early as 2011 and recently referred to in a post on his blog, Our low risk (low volatility) world.

Low volatility is a variation on the prosperity argument used by Minksy to start the cycle of speculative excess. Low volatility lulls investors into thinking risk is actually lower than reality just like prosperity or no economic downturn will cause bankers to change lending practices. Because perceived risk is lower, there is a willingness to increase leverage and increase investment in riskier assets. Risky assets are bid higher which are then used as collateral for further leverage. This volatility argument is separate from the reach for yield because of low interest rates. Risk-taking on low volatility makes the financial system more fragile.

The problem of misperception by investors with respect to measured risk and actual risk is real. Investors may be placing too much stock in recent volatility and too much emphasis on standard deviation as the right proxy for risk. Low volatility today does not mean low volatility tomorrow. Low volatility today will create behaviors that will lead to more risk tomorrow. The smart investor should be looking for long vol or divergent strategies that will profit from an increase in volatility.

Related Posts

Anatomy of a Tough Month for Trend-Followers: Tariff Shocks & Volatility Spikes

It is often said that trend followers provide “crisis alpha.” This means that market stress often benefits their strategies. This follows logically as moves get larger, coordinate together, and run consistently, trading becomes easier. These managers quickly caution that they do not always provide this negative correlation. Price action can swing unpredictably against long-standing trends […]

Time-varying correlation – Diversification benefits are dynamic

What is the correlation between two assets? The correlation is critical because it is the driver for any diversification decision. The better question is, “What is the correlation now, and what can it be in the future?”. Correlations are often time varying and regime specific. In bad times, correlations rise, so the diversification expected is not present when you need it. This phenomenon requires more thinking about tail risks and how to best address them.

The “3 by 5 Index Card” on What You Need to Know About the February VIX Spike

University of Chicago professor Harold Pollack in an interview a few years ago mentioned that the best money advice can fit on a three-by-five inch index card. He was then challenged to write the card. His financial advice went viral. We follow this tradition by focusing on a simple “three-by-five index card” on the VIX volatility spike earlier the month.