Numbers and statistics are a funny thing. They usually don’t lie and are not fake. You can misinterpret them, but numbers tell a story and it is the job of the investor to either accept the story or come up with an alternative.

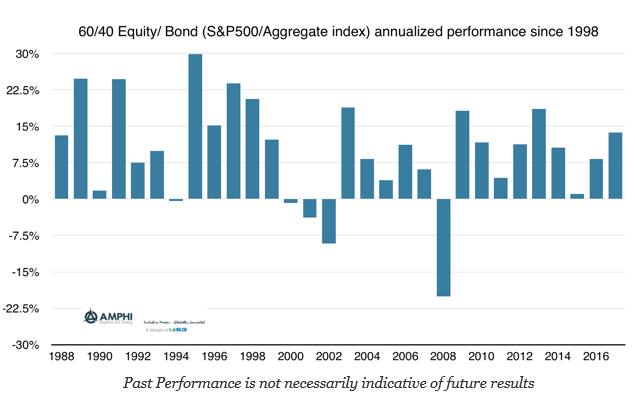

For many investors, there has been a strong adherence to the 60/40 mantra. The mantra says that 60/40 will protect an investor in a downturn and provide strong risk-adjusted returns in all environments. There can be variations on this theme, but 60/40 has often served as the core allocation for many investors. For 2017 this portfolio combination was again a winner. The 60/40 SPY/AGG (using index total returns) combination generated a return of 13.74% in 2017 which was above the average of 9.86% for the last 30 years.

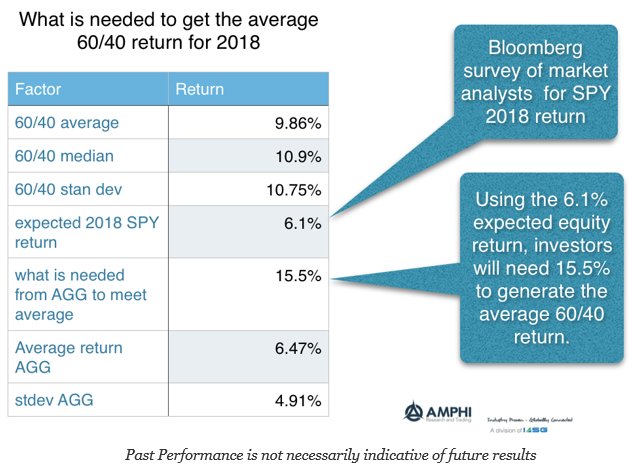

It is natural to keep with this winning strategy, but it might be good to run some scenarios to see what you will need in 2018 to generate the long-term average annual return for a 60/40 combination. Do not expect a repeat of 2017.

We used the average forecast for 2018 equity returns (SPY) from a Bloomberg survey as a base equity number and worked backwards to calculate the returns necessary from the AGG index to generate the average annual 60/40 return over the last 30 years. In this case, the Aggregate index would have to generate over 15% next year. That is unlikely to happen. It would be over 2 times the average AGG return and just under 2 standard deviations from the average over the last 30 years. This return would be without the help of the higher currents yields over the last 30 years.

Even with the expected SPY returns, just to generate a 6% return for the 60/40 portfolio would require a significant decrease in rates since yields are so low. To get the average return for a 60/40 portfolio, equities will have to exceed the high end of the SPY estimates from analysts and the Aggregate bond index will have be close to its average return of 6.5%. Even to reach expected portfolio returns of 7% will require above average returns in equities and a positive return year for bonds. Most of these scenarios are not likely.

One of the only likely scenarios for better returns is for asset allocation adjustments based on strategy diversification focused on absolute return. This means high alpha strategies or dynamic beta strategies that can exploit moves in equities and bonds regardless of their market direction. If you want to beat your target return and the 60/40 average, you will need to look outside the usual asset allocation box.