Inflation is becoming a greater concern with many investors, but forecasters are more mixed with their views. The latest CPI number posted a 2.1% year over year change and the core CPI showed a 1.8% change. CPI has been above 2% for 8 of the last 12 months; however, both the CPI and core CPI changes were higher last January. These numbers are stabilizing at a higher level around 2% although there is not a run-away threat with the actual numbers or market expectations.

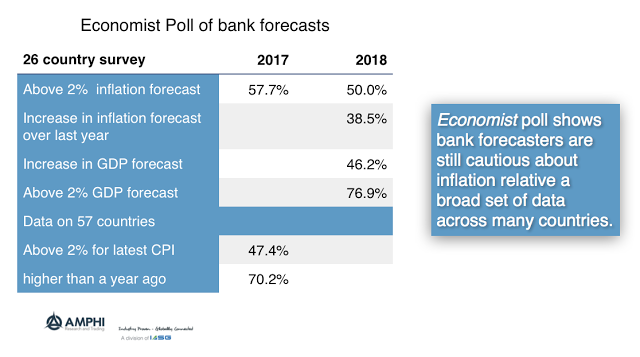

For investors, the question is whether to trade against expectations or stay the course with an assumption of moderate inflation approaching and hovering around 2%. The bet can be place in global context through looking at the Economist Poll of bank forecasts for 26 different countries. 50% of the forecasts are for inflation to be above 2% and 38.5% of the country forecasts show an increase over last year. Less than half the country forecasts show an increase in GDP growth; however, just over 3/4ths expect growth above 2%.

The actual inflation numbers of a broad survey of 57 countries show less than 50% having inflation above 2% but 70% have inflation higher than a year ago. Markets expectations concerning growth during the second half of the year were biased low. The low growth forecasts errors will likely carryover to inflation. Based on stronger growth and the lagged impact of any liquidity tightening, inflation across a broad set of countries will be better than 50% and our estimate is that over 2/3rds of countries will see a further increase in inflation over last year.

Related Posts

2025 in Review: Markets, Policy, and the Path Forward

History never repeats itself, but it often rhymes. This is even more so the case this year, as Trump began his second term with similar but different disruptions to the markets. Rising stocks, normalizing inflation, and the AI boom took center stage. We discuss some of the key events below and try to anticipate where […]

The Bankruptcy Cycle Returns: Delayed Failures and the Cost of Easy Money

Proper forest management requires clearing dead brush, protecting high-risk areas, and conducting controlled burns. As January 2026 approaches, marking the one-year anniversary of the devastating Southern California wildfires that destroyed over 16,000 structures, we examine the mistakes made and how those lessons apply to the financial markets. Much like forest fires, risk can be mitigated […]

How Irrational Is It? Valuation Ratios and Bubble Risk

For anyone who has ever ridden a roller coaster, the distinct sound of the chain nearing the top of the first drop echoes in our ears. Click, click, (slower) click…. Anticipation builds right before we experience the massive first drop, picking up speed on the way down. If only the equity markets provided the same […]