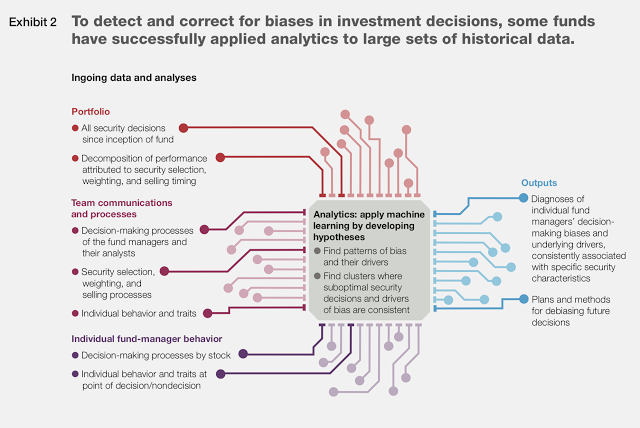

McKinsey and Company published an interesting paper on the use of AI in asset management called, “An analytics approach to debiasing asset management decisions”. (Hat tip to Tom Brakke for mentioning the article in his newsletter.) This paper shows the powerful use of analytical tools to extract hidden biases in investment management decision-making. Employing large data sets of manager decisions, companies are finding a wide set of behavioral biases identified in economics present with their decision-making.

Regardless of how smart the talent, biases can be deeply embedded in decision-making. These biases are often hidden from direct views because there was no systematic analysis of the data. Nevertheless, if they are found, there is a chance that decision-making can be nudged in the right direction. For example, if there is a confirmation or anchoring bias, the data can find the “bad” behavior, and procedures can be adopted to eliminate them.

This is a great use of artificial intelligence and data mining, but it begs the question of why rely on individual or committee decision-making in the first place with investment management. Systematic investing featured in quant programs, by their very nature, debiases decision-making. If there is confirmation bias, rules can be used to reduce it. If there is a bias to hold losers and sell winners, rules can be developed to reverse this tendency.

This does not mean that systematic programs are devoid of bias. It just means that the biases through a rules-based system are transparent. If they are present, it is because someone put them in the program. Any known behavior biases can be addressed directly. Perhaps the greatest value of systematic investing is not the development of any one special strategy but a holistic disciplined approach to ensure repeatable success.

Related Posts

Cayler Capital | April Performance Commentary

After finishing off one of the wildest quarters of my trading career, April managed to take the cake. For those that missed it (not sure how you possibly could have), oil settled negative $37. The effects of this were immediate: risk barometers had to be recalculated, option models switched, and most importantly was the immediate […]

Mike Lombardi, football coaching and investing

I am not a football fanatic, but I picked up this book on a recommendation and was amazed by Lombardi’s insights on leadership and management. Mike Lombardi is long-time football executive and media analyst. The book focuses on Bill Belichick and the New England Patriots, but his conclusions could apply to any money management firm. A good money management firm is successful because it acts like a well-disciplined organization with a common purpose. That is no different than a competitively run sports organization. Lombardi finishes his book with five key recommendations for firm success that are worth presenting in bold.

“The Emeril Lagasse Theory” – Practical knowledge and culture is not often transferable

After hundreds of discussions with hedge fund managers, I am still surprised that there is a fear of revealing investment processes under the assumption that someone will steal their ideas and intellectual capital. There are few investment styles that are truly unique and special. What is special is still strategy execution – the practical process of delivering returns. Skill is with the decision-making execution of information and strategy.