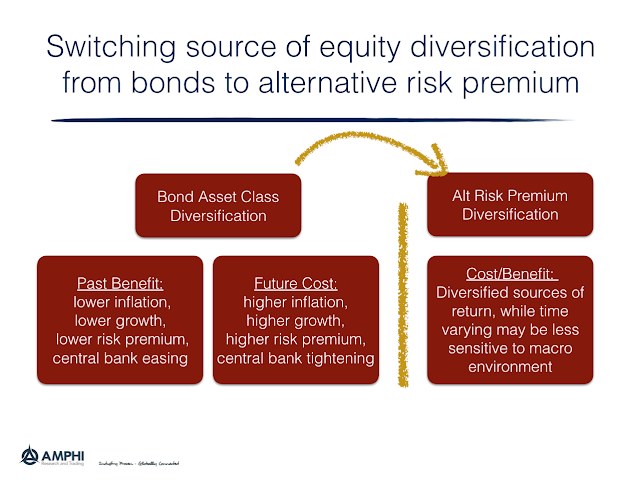

Investors want diversification from their equity exposure. This desire for diversification increases with uncertainty and with expectations of an equity decline. The big question is, how or where are you going to get this diversification? The diversification winner for the post Financial Crisis period has been simple, US bonds. Bonds have been an asset that generated a good rate of return with lower volatility and a negative correlation with equities. You could not ask for a better diversifier. Unfortunately, the investment environment is changing and the benefits from bonds may no longer be available, so there is an increased desire to find new diversifiers.

An effective alternative diversifier could be a portfolio of alternative style risk premiums. No investor should divest all of their bond exposure, but alternative risk premium (ARP) strategies may offer a different form of diversification safety.

Think about the cause of the core bond diversification boost. Bonds benefited from low inflation, declining risk premium, and central banks that wanted to push rates lower. This combination led to good returns that were uncorrelated with equities. Now inflation is higher, central banks are implementing or contemplating QT policies, and risk premia are expected to rise. The underlying bond factor environment is less favorable.

Diversification going forward can be achieved holding alternative risk premia across momentum, carry, value, and volatility to name a few. These alternative risk premiums can be executed through swaps which can be done as an overlay on bonds.

Will these style premiums perform better than bonds? It is not clear and looking at past performance may not provide a perfect answers. What we do know is that an investment in a style risk premium will be by definition uncorrelated with market betas. Investors would be switching the risk factors driving returns and that can help if market beta risk is a concern.