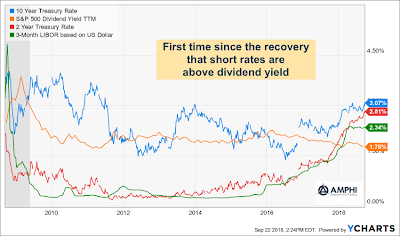

Short-term interest rates are now above dividend yields for the first time since the Financial Crisis. This could be a big deal. Investors can now hold short-term bonds and receive a higher carry return than holding dividend-paying stocks. The cost of holding cash is now less than holding dividend stocks.

There is a long history of research that suggests that high dividend yields are indicative of cheap stocks and dividend yield are a strong contributor to total return, but we are interested in the relative relationship with yields. This issue is a variation of the old Fed model discussions of richness and cheapness in stocks. The current condition of rates higher divided yields could suggest that stocks are priced high, but we need more historical context.

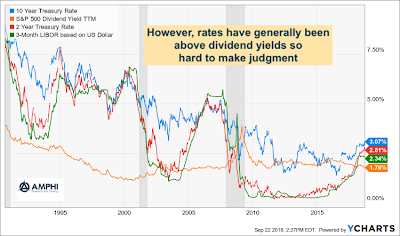

A look back to 1990 suggests that fixed income yields above dividend yields are not the exception, but the norm. In fact, one can argue that the post crisis period is the time frame that is unusual.

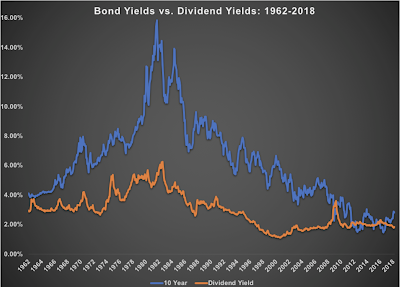

Going even further back in time suggests more of dividend yield puzzle of what is the relationship between dividend yield and rates. The last ten years were exceptional. But, in the first half of the twentieth century, dividend yields were higher than short rates. This relationship shifted in the 1950’s. This was certainly before the craze in buybacks which could have served as a substitute for increasing dividends.

While dividend yields are not as volatile as interest rates, there have been distinct periods of dividend and bond yield changes. The 50’s to 70’s, a period of rising inflation, saw bond yields moving higher and dividend yields declining. The still higher inflation period of the 70’s saw dividend yields and bond yields both rising. The Great Inflation Decline between the 1980’s and 2000 produced lower dividend yields and bond yields. This was also a period of increased buybacks. The last 20 years saw stable to higher dividend yields but bonds lower. We are now in a bond yield higher and dividend yield stable environment without counting buybacks. Still, this transition may not provide guidance on the stock market.

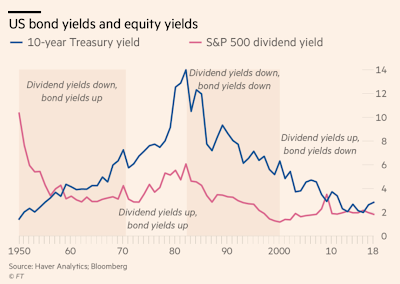

There are three major conclusions from this data. One, do not put stock in short time periods for analysis. Two, we may be looking at a different stock bond environment as signaled by the rate dividend relationship. Three, the relationship between rates and dividend yields may just does not tell us much on the future direction of stocks. All facts may not be meaningful.