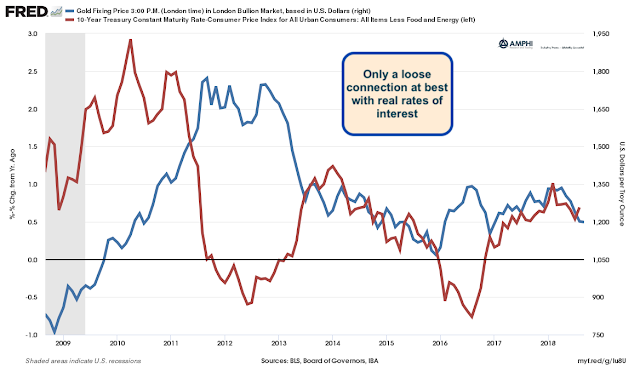

We have written about the surprising lack of gold price gains with the surge in inflation. A reader has commented that it is the real rate of interest that is important, not inflation. Unfortunately, the data does not seem to show a close relationship.

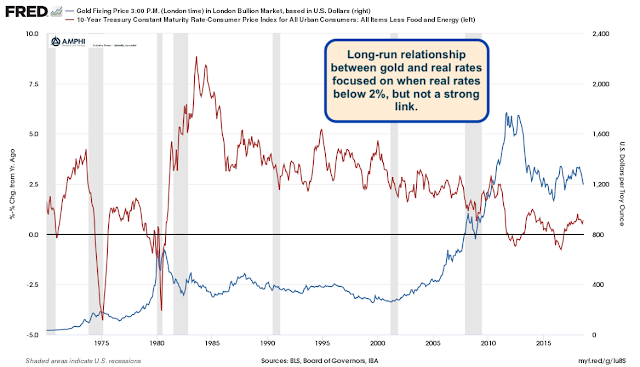

If the real rate of interest is positive there is a cost with holding a non-interest bearing asset such as gold. Similarly, if the real rate of interest is negative, the opportunity cost of holding gold is diminished. A graph of the real rate in the US versus gold seems inconsistent with this opportunity cost story. While there is a relationship around some key periods, the gold real rate story is not strong in the short-run. In the longer-run, the surge in gold was tied to a decline in the real rate, but the relationship is not linear. There will be surges in gold prices during a crisis or when there is a decline in real rates below 1-2%. It is the surprise in inflation that matters.

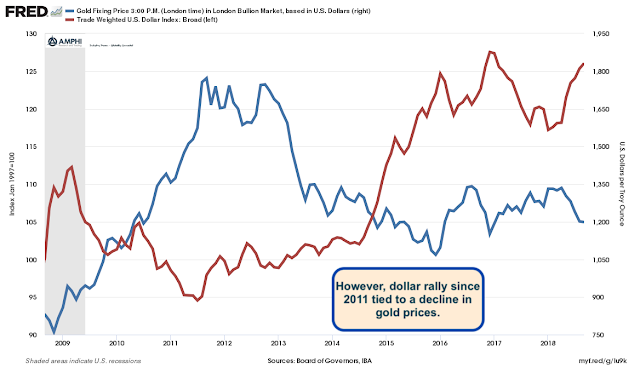

The relationship between gold and the dollar is stronger as evidenced by the graph. The increase in the dollar more closely matches the decline in gold prices during the post Financial Crisis period.

Gold is closely tied to expectations across a number of factors, and the emphasis on each factor is not constant.

Related Posts

Iran, Venezuela, and the New Global Oil Order

Recent events remind us that balance in energy markets can be delicate. A conflict in the Middle East and the removal of a sitting President in Venezuela resulted in sharp moves across the energy industry in early 2026. Currently, the Iran War is creating havoc in crude shipments, affecting the world. While trouble in that […]

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Decoding Metals Price Action

Markets often communicate more clearly through price action than through headlines. The dramatic surge in metals contracts is sending a powerful signal, but what exactly is it telling us? Traders frequently monitor inter-market relationships for early warnings. When one asset class moves unusually, it can ripple across the system or reveal deeper structural issues. In […]