Everything you have heard about yield curve inversion is true; nevertheless, everything that is true may not harm your investments. Yield curve inversion is a good predictor of recession, and there is a link between this inversion, recession prediction, and equity declines. However, being the first to react to flattening or inversion may not win your portfolio success.

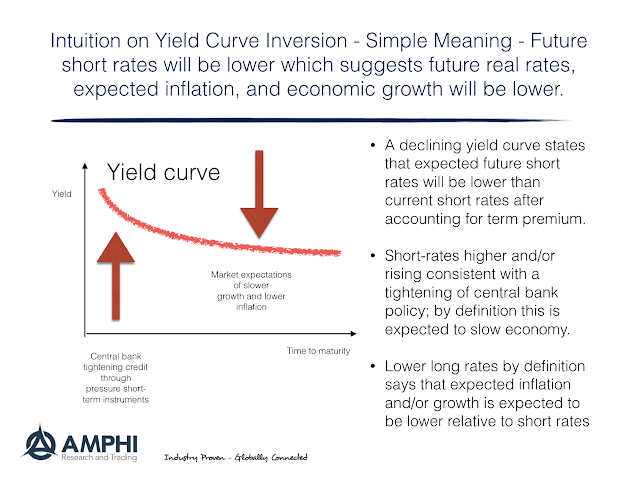

The critical question is determining what the inversion signal represents between current and longer-term expectations. In simple terms, short rates tell us something about current Fed policy, currently expected inflation, and recent economic growth. Longer rates tell us something about Fed policy, expected inflation, and current economic growth, but over longer horizons.

Hence, after accounting for any term premium, the steepness or inversion of the yield curve tells us something about relative expectations, no more or no less. A greater yield slope translates to more significant divergence between short and longer-term expectations. An investor has to ask the simple question, “Do I agree with the relative expectations in the curve?” Given what the market is telling you, the next question is whether you should act on this view today. An inversion in this framework should be viewed dispassionately.

Related Posts

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

The Evolution of Trading from Systematic to AI

Is AI the next step in the evolution of trading? History proves new tools storm the markets, then high adoption erases their edge. What can futures trading history teach us about AI’s trajectory? The 1980s: Rise of Rules-Based Trading Building on simple regression models that aimed to identify patterns across sectors, the 1980s showed that […]