There has been a lot of discussion on the lack of success with momentum and trend-following strategies. There is little doubt that there has been greater dispersion in returns across managers. There have been winners and losers with disappointment focused on some larger high profile firms.

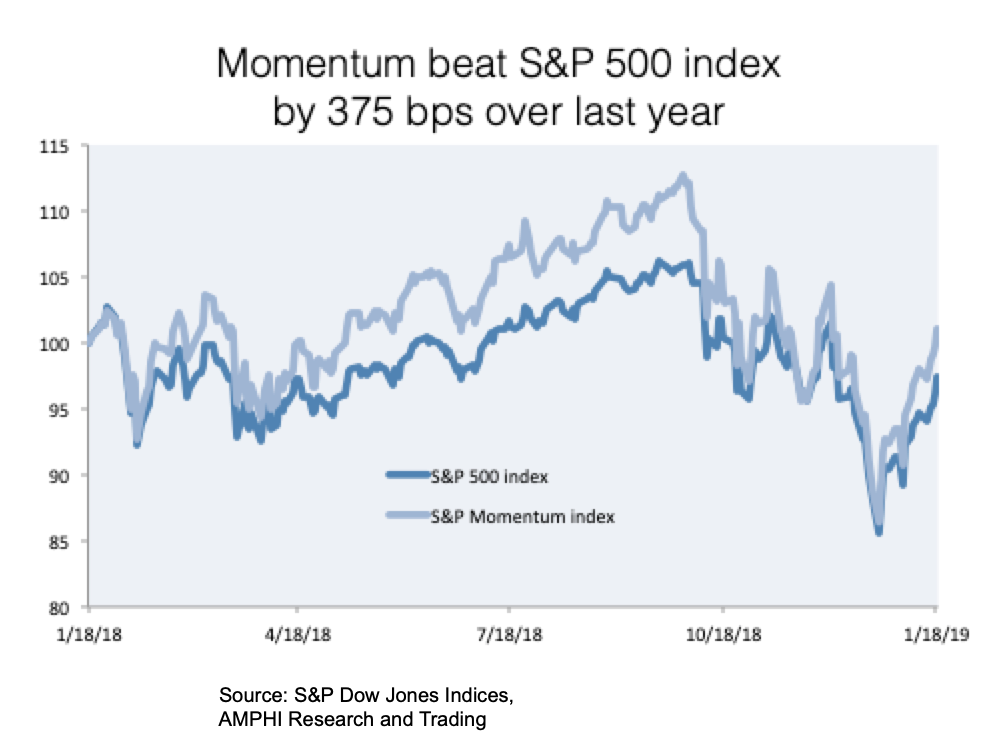

Small differences in models have lead to large changes in return. This is what happens when momentum is not smooth. Smoothness is defined as the trend to volatility ratio, or the switching of return patterns for classic momentum filters. Nevertheless, the strategy is sound. Just look at a simple momentum strategy over a relatively difficult year.

This SP/Dow Jones momentum index, using the large cap 500 equity set, is compared with the SPX index. The overall return impact has been positive over the last year. Clearly there are some expected patterns between the two indices. One, when the market trends in one direction, momentum will exaggerate the market direction for the better and worst. Two, momentum reversals lead to givebacks versus the market weighted index. Three, a long-only momentum index will exploit the long-term positive equity direction. Four, there is a cost with momentum, higher volatility and a return penalty during transitions.

Momentum strategies work, but part of the risk premia for holding the strategy is the cost of transitions. Investors who are late entrants to a momentum strategy will face the highest risks. Momentum should be a core part of asset allocation or entry for this risk premia exposure should be during periods of poor performance. Timing on superior past performance is risky.

Related Posts

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

The Evolution of Trading from Systematic to AI

Is AI the next step in the evolution of trading? History proves new tools storm the markets, then high adoption erases their edge. What can futures trading history teach us about AI’s trajectory? The 1980s: Rise of Rules-Based Trading Building on simple regression models that aimed to identify patterns across sectors, the 1980s showed that […]