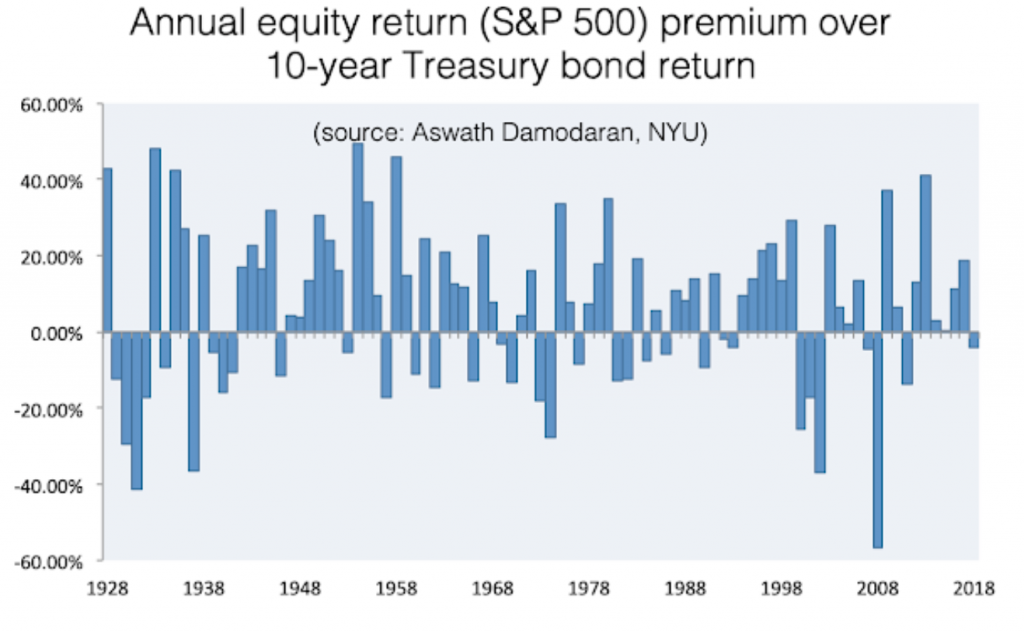

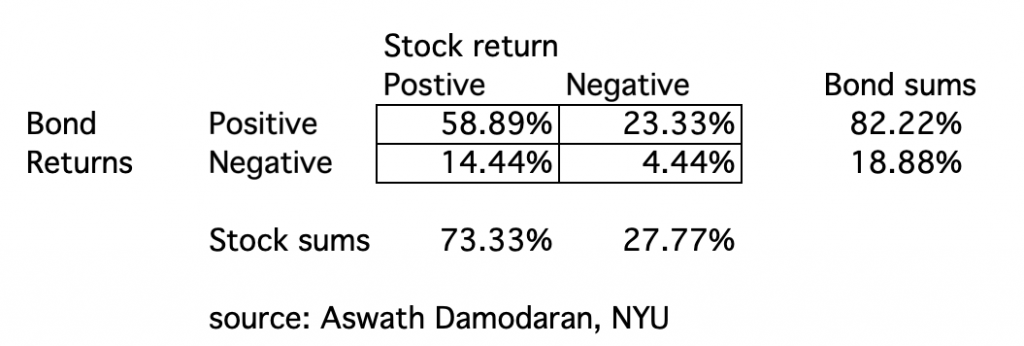

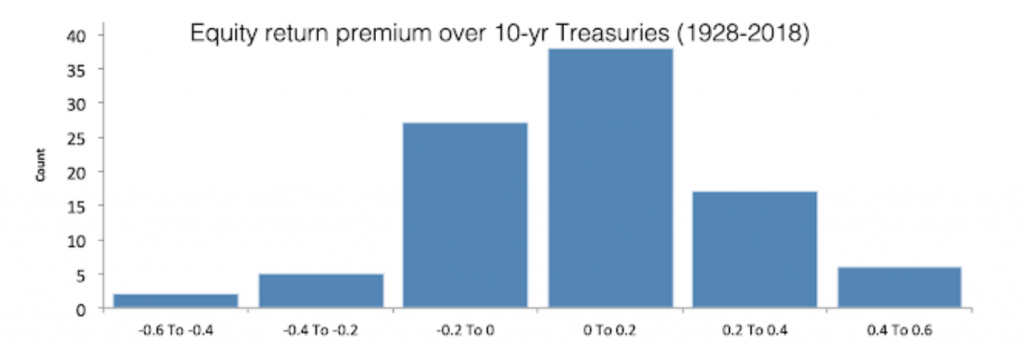

Many investors don’t appreciate that 2018 was highly abnormal for asset allocation. First, the annual excess return from holding equities is generally positive with the exception during recessions. 2018 was not a recession year. Yes, there was a slowdown in the fourth quarter, and growth expectations have slowed but the numbers do not suggest a recession at this point. Second, the likelihood that both stocks and bonds will be negative in a given year is very unusual. There has only been a 4.44% chance of this occurring over the last 90 years using the SPX and 10-year Treasury returns. It is highly unlikely that we will see a similar year in 2019. There have only been seven periods when the equity premium was negative for two or more years in a row.

Additionally, the equity return premium over bonds is usually large. The arithmetic average is about 6.25 percent with a standard error of 2.25 percent.

Any bias should be to still hold strong equity risk exposure although a bias away from a 60/40 base case is warranted given the slower economic growth, uncertainty about liquidity, and higher volatility. The historical numbers always justify holding equities unless there is an exceptionally poor macro environment.

After hundreds of discussions with hedge fund managers, I am still surprised that there is a fear of revealing investment processes under the assumption that someone will steal their ideas and intellectual capital. There are few investment styles that are truly unique and special. What is special is still strategy execution – the practical process of delivering returns. Skill is with the decision-making execution of information and strategy.

All hedge funds are not created equal as the return box chart shows for the post Financial Crisis period. There is a significant amount of dispersion across hedge fund styles. Over the period 2009-2018, the difference between the best and worst hedge fund category is almost 7 percent after we account for global equities and bonds.

The attraction to private equity and other less liquid alternatives is clear from the Guide to Alternatives by JP Morgan Asset Management. The return profile is much higher for private equity and debt funds than more liquid alternatives and global bonds; however, the dispersion in returns is multiples higher than what can be expected from other public categories.