The trend is with risky US assets which is not what we saw in the fourth quarter of last year. The reasoning for risk-on is sound; equity volatility has been reversed and financial stress has fallen. These effects have dominated the US market and have had a stronger impact on riskier assets.

Nevertheless, there are bad things happening in the world. It can be political or economic, but don’t worry about the US because everything is right here. If you read the news headlines, you would not believe it, but if you follow markets you are in an alternative universe. In the financial alternative universe, small cap, growth, and value indices are all do well and offsetting much of their declines in 2018. Stocks are good and bonds are acting like diversifiers. Earnings have shown strong year-over-year gains and the future, which is suggesting lower expectations, does not matter.

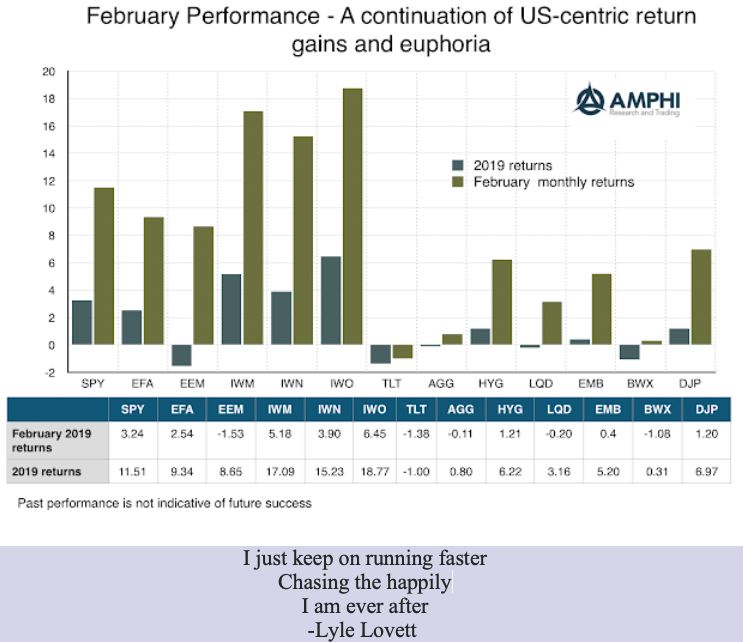

Economic data of a mixed growth story is not being fully discounted. The data for March is not compelling. University of Michigan consumer expectations are below levels from 2018. ISM purchasing manager’s PMI numbers are good, above 50, but showing downward momentum. Investors are “chasing the happily they are ever after”. It is an easier story to believe.

After hundreds of discussions with hedge fund managers, I am still surprised that there is a fear of revealing investment processes under the assumption that someone will steal their ideas and intellectual capital. There are few investment styles that are truly unique and special. What is special is still strategy execution – the practical process of delivering returns. Skill is with the decision-making execution of information and strategy.

All hedge funds are not created equal as the return box chart shows for the post Financial Crisis period. There is a significant amount of dispersion across hedge fund styles. Over the period 2009-2018, the difference between the best and worst hedge fund category is almost 7 percent after we account for global equities and bonds.

The attraction to private equity and other less liquid alternatives is clear from the Guide to Alternatives by JP Morgan Asset Management. The return profile is much higher for private equity and debt funds than more liquid alternatives and global bonds; however, the dispersion in returns is multiples higher than what can be expected from other public categories.