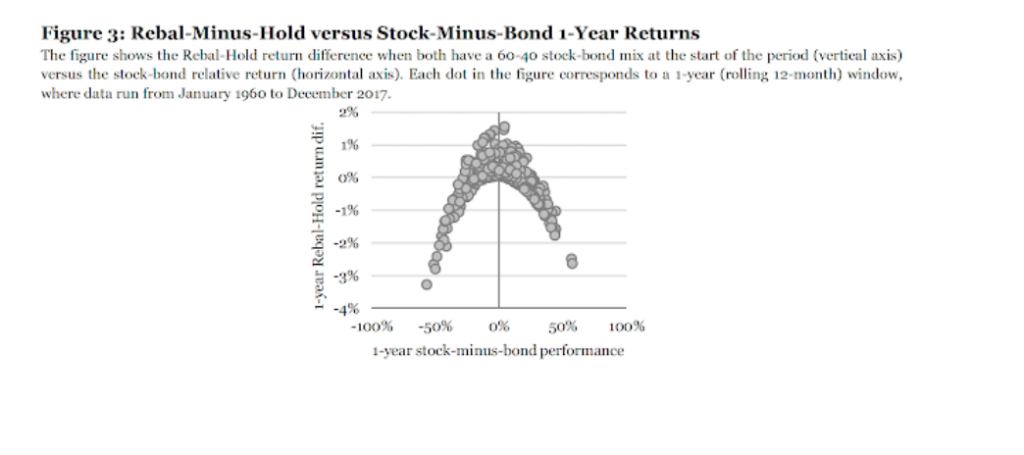

Rebalancing has become an essential tool for portfolio management. Nevertheless, market return patterns will affect the return impact of rebalancing. Regular rebalancing is a mean-reverting strategy. For example, suppose there is a simple 60/40 stock/bond portfolio. In that case, stronger stock performance will cause the allocation to deviate from the strategic allocation and lead to a higher allocation to stocks over bonds. A rebalance will take money away from the better-performing asset and give it to the underperforming asset. It sells winners and buys losers regularly. See “Strategic Rebalancing” by Granger, Harvey, Rattray, and Van Hemert

Rebalancing may seem like an innocent enhancement strategy under regular times, but if there are market trends, rebalanced portfolios will show poorer performance than a buy-and-hold strategy. It will affect drawdowns and volatility. Take the simple market extreme during the Financial Crisis; rebalancing would have continued to add exposure to stocks even during the extended downturn, taking money away from the better-performing bonds. In essence, a rebalancing strategy generates negative convexity for a portfolio.

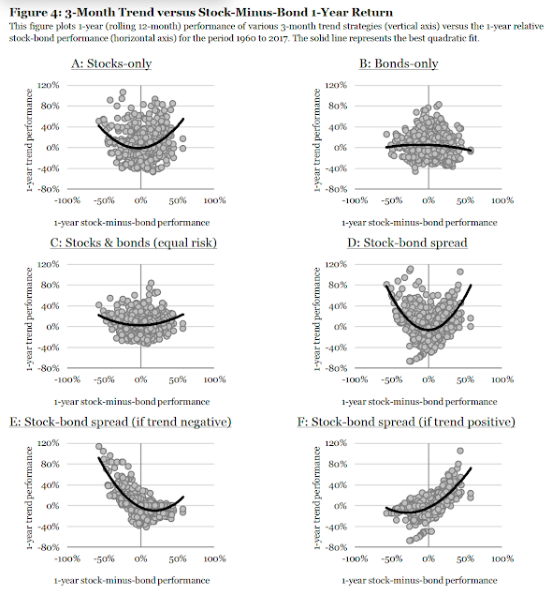

A simple marriage between rebalancing and trend-following is consistent with holding winners and not giving to losers. This will offset the impact of rebalancing drag. While the effects of strategic rebalancing will be minimal during periods of calm, there will be a substantial benefit if we move to extremes. Applying discipline will allow for positive portfolio convexity at the right times.

Related Posts

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

Bowmoor Capital – A Different Approach to Trend Following

Competing head-to-head to outsmart others doing the same strategy is often a tough road. In trend following circles, giants like Man AHL, Winton, and Aspect dominate assets under management. This enables them to hire top PhDs, deploy better technology, test ideas rapidly, and outspend smaller players on sales and marketing. So how can a smaller […]

The 6 Biggest Myths About Diversification and Non-Correlation

“If everything in your portfolio goes up and down at the same time, you have a bad portfolio.” This simple but powerful observation from Mark Rzepczynski, former CEO of John W. Henry & Company, is one I think of often – for both my customers and my own investing. A losing position in your portfolio […]